Loans are a popular means of financing in a group of companies, both to cover short-term cash gaps and to implement long-term projects. In order not to face claims from tax authorities, a choice is often made in favor of interest-free loans. But are interest-free loans as harmless as it seems at first glance?

TaxCOACH experts analyzed claims from fiscal authorities that arise when issuing (receiving) exclusively interest-free loans. And not only in the group of companies, but in general, in relation to any possible options.

For analysis, we took all court cases on tax disputes that reached the cassation court from the beginning of 2021 to March 2020, in which the words “interest-free loan” were heard in any way.

The results turned out to be very interesting. Let's try to trace why and when business entities use interest-free loans, and in what manner the tax authorities react to them.

Cases in which relations involving gratuitous borrowing were considered can be divided into several categories.

Unjustified tax benefit cases

Almost half of the cases concern unjustified tax benefits associated with the illegal receipt of VAT deductions (refunds) for transactions with “one-day companies.”

Interest-free loans in such disputes are the basis for tax authorities to make conclusions about:

1. The transit nature of the movement of funds. That is, the person who performed the services is only a nominal person who organizes formal document flow with the taxpayer.

2. Withdrawal of funds from the business. This conclusion is related to the previous and subsequent ones. In most cases, tax authorities pay attention to the lack of return of funds as evidence of the withdrawal of funds to third parties or interdependent entities. In addition, the non-repayment of the loan is assessed as an integral attribute of a “fly-by-night” loan.

3. Interdependencies of the parties to the transaction. It is obvious that the transfer of funds free of charge (without interest) has no economic purpose for the creditor; accordingly, such relations are not typical for independent entities.

4. Bad faith of the counterparty. The presence of facts of issuing interest-free loans is, in the eyes of the tax authorities, one of the general characteristics of the bad faith of the counterparty.

In many ways, these findings are intertwined with each other and used together. And the very presence of interest-free loans, especially those not repaid at the time of the audit, is assessed by the tax authorities as a sign of suspicion of the counterparty, other transactions with which require attention.

Terms of interest-free loans

When drawing up a contract, you should thoroughly study all the clauses included in it. After all, the absence of interest does not at all relieve you from the responsibility that you will acquire by entering into a borrowed relationship.

Traditionally, any sample loan agreement includes the following information :

- Item. If it is money, indicate the amount (both in numbers and in words), as well as the currency; if these are things, a list of them is written down (in the text or in the appendix);

- Interest. If % is missing, then this must be written down to avoid possible controversial situations;

- Duration of the relationship. If the loan is indefinite, then the repayment date will be determined by the lender’s requirement - by law, the borrower is given 30 days from this moment;

- Purpose: targeted or non-targeted;

- Payment method: how the loan will be provided and how it will be returned (cash - non-cash, lump sum - tranches - according to schedule);

- Responsibility. Particular attention should be paid to penalties: sometimes the absence of interest implies huge fines for late payment and non-payment.

Gratuitous loans in cases of artificial division of business

Many of the above methods of using gratuitous loans are found in cases of artificial division of a business and are presented by the tax authority as evidence:

- interdependence of business entities operating as a single business. The MKD management company created an interdependent contractor to take advantage of the specialized VAT benefit. The tax authority established the identity of the companies’ activities, and interest-free financing did not raise any doubts in the court’s mind about the creation of a scheme for artificial fragmentation (Resolution of the Arbitration Court of the Volga-Vyatka District dated March 12, 2019 in case No. A43-47773/2017).

- lack of independence and control of the participants in the loan agreement (Resolution of the Arbitration Court of the Far Eastern District dated February 13, 2019 in case No. A59-5764/2017).

- the presence of a single financial center, which controls the entire group of companies. The proceeds of controlled legal entities were immediately transferred to the beneficiary (IP) in the form of interest-free loans that were not repaid. The courts equated these amounts to the revenue of the individual entrepreneur, and therefore the individual entrepreneur lost the right to apply the simplified tax system. (Decision of the Supreme Court of the Russian Federation dated November 13, 2021 in case No. A27-2411/2016).

In the well-known KFC case (Resolution of the Arbitration Court of the North Caucasus District dated 02/26/2020 in case No. A32-50460/2017; Resolution of the Arbitration Court of the North Caucasus District dated 02/05/2020 in case No. A32-53098/2017) interest-free loans were used as a way financing of interdependent persons, which was perceived by the tax authority as one of the proofs of the non-independent nature of business activities by business entities. In addition, funds received as gratuitous loans were issued with the purpose of “payment for semi-finished products” with subsequent receipts for “return of payment for semi-finished products.” Thus, the company tried to hide gratuitous financing of current activities in a group of companies without achieving a business goal of obtaining economic benefits on the part of the lending organization.

Accounting

The debtor must keep records of the loan on the basis of PBU 15/01 “Accounting for Loans”, established by Order of the Ministry of Finance No. 60n dated August 2, 2001. Calculations will be recorded on accounts 66 and 67. Debt is taken into account in the valuation of acquired assets (clause 3 of PBU 15/01).

The resulting assets must be capitalized at a value determined using the same algorithm that is used when valuing similar objects. However, an accountant can make his job easier. For the posting price, you can take the amount specified in the agreement. If no amounts appear in the contract, you can take the cost stated in the invoice.

The transfer of ownership rights to objects is considered a sale on the basis of paragraph 1 of Article 39. The operation is considered an object of taxation. In particular, it is subject to VAT.

Often, with a commodity loan, the debtor receives one item and returns another item with similar characteristics. In this case, the real value of the transferred assets may differ from the real value of the returned items. The difference that arises is attributed either to income or to expenses, depending on its positive or negative value. Differences are accounted for on the basis of PBU 18/02, approved by Order of the Ministry of Finance No. 114n dated November 19, 2002.

The lender must also take into account the commodity loans provided. Accounting is carried out on the basis of PBU 19/02, approved by the Ministry of Finance No. 126n dated December 10, 2002. Paragraph 3 of this act states that a trade loan will be considered a financial investment. The amount must be recorded in account 58. The loan is assessed based on the actual value of the transferred assets. After classifying things as financial investments, the cost of the objects is compared with their cost during regular sale without VAT. The resulting difference is attributed either to income or expenses.

Gratuitous transfer of funds covered by a gratuitous loan agreement

When transferring funds under a loan agreement, whether paid or gratuitous, it is important to understand that this operation must be repayable. Otherwise, it is difficult to disagree with the tax authorities that such a transaction is a gratuitous transfer of property, subject to income for the receiving party.

...The funds received under an interest-free loan agreement were recognized as gratuitously received property, since the taxpayer did not provide any documentary evidence of the existence of borrowed legal relations, and therefore these amounts were subject to inclusion in non-operating income. (Resolution of the Arbitration Court of the Ural District dated February 13, 2019 in case No. A07-30518/2017).

It should be noted that in cases where the tax authority believes that the relationship under the loan agreement is of a formal nature, and therefore the loan agreement covers a gratuitous transfer of property, the facts of the remuneration of the agreement and the return of funds by the time the dispute is considered may play a key role.

Thus, in case No. A76-24391/2018, the court agreed with the taxpayer about the illegality of additional income tax charges on the amount of funds received under the loan agreement. As the court pointed out, it followed from the terms of the agreement that the loan was interest-bearing, and therefore it cannot be recognized as a gratuitous transfer of property.

Consequences of violation by the borrower of the loan agreement

The consequences of the borrower ignoring the terms of the loan agreement are regulated by Art. 811 of the Civil Code of the Russian Federation, which reads:

- If the borrower does not repay the loan within the prescribed time, interest is charged on the amount of the debt in accordance with clause 1 of Art. 395 of the Civil Code of the Russian Federation, from the date of the due date for repayment of the loan until the day of actual repayment of the debt.

- If the loan agreement establishes the repayment of the loan in installments (in installments), then if the borrower fails to comply with the deadline for repaying the next part of the loan, the lender has the right to demand early repayment of the entire remaining debt along with interest accrued before the loan repayment date.

0 0 vote

Article rating

Free loan as a way to pay dividends

The next case deserves special attention, since we admire both the resourcefulness of the entrepreneur and the creative approach of the tax authority in identifying the tax evasion scheme.

The court considered a controversial situation in which a member of a group of legal entities received both interest-bearing and interest-free loans from its legal entities. The funds received from loans were periodically partially spent on repaying previously incurred loans. But the total amount of debt gradually grew. A participant in a society would have a kind of pyramid of debts. Your own “MMM” for yourself.

The tax authority, having established that the funds were spent by the founder for his personal needs and were not used in business activities, came to the conclusion that, in fact, the funds received free of charge were his dividends from participation in the group companies.

The court supported the tax authority. (Resolution of the Arbitration Court of the North-Western District dated January 31, 2019 in case No. A26-3394/2018).

Requirements for the contract

You can draw up a loan agreement yourself, as it is not particularly difficult.

Key points:

- complete information about the parties indicating their full names, passport details, addresses;

- the amount of the loan, indicated in numerical and verbal terms;

- method of transferring money (cash, by crediting a card, bank account);

- is interest payable, if so, in what amount;

- the period after which the debt must be repaid;

- the procedure for returning money, as well as the possibility of early repayment of debt. You can provide for the possibility of paying in installments, then you should attach a payment schedule or simply indicate the frequency of payments (for example, monthly or quarterly);

- moment of termination of obligations.

If new circumstances arise, additions or changes can be made to the contract by formalizing them in the form of an additional agreement. It must be compiled in two copies. And you should not allow corrections in it. A sample agreement can be downloaded below.

Compensation of contractual relations

A loan between citizens can be free of charge. This means that the borrower returns to the lender after the agreed period exactly the amount that he took for temporary use. If the contract is concluded on such terms, then this must be indicated.

The lender has the right to receive interest from the borrower for the loan provided by him. Their sizes are established by agreement of the parties and must be specified in a written document. If the agreement specifies remuneration without a specific amount of interest, then the refinancing rate in effect on the date of its conclusion is taken for it (Article 809 of the Civil Code of the Russian Federation).

Responsibility of the parties

Drawing up a written document acquires particular importance if the borrower fails to fulfill its obligations under it:

- failure to return the amount borrowed for use;

- repayment of the debt with interest overdue the agreed period.

In such circumstances, the borrower is held liable in the form of paying a penalty. Its amount is determined by the parties by mutual agreement and is accrued for each day of delay. But the total amount of the penalty should not be equal to or exceed the amount of the debt.

It is advisable to provide for all possible cases of violation of the terms of the agreement by the parties and liability in case of their occurrence.

Lack of business purpose when issuing an interest-free loan

We believe that the following incident, which occurred with a 17-year-old entrepreneur, should be highlighted separately. The tax authority (Resolution of the Arbitration Court of the West Siberian District dated January 18, 2019 in case No. A67-7866/2017) conducted an on-site tax audit of an entrepreneur who received multimillion-dollar loans from some and transferred to other companies. The tax authority assessed additional personal income tax on the funds received, indicating that the loan agreements do not reflect the actual economic meaning of the transaction, are not due to reasonable economic reasons (business purposes), were drawn up for the creation of formal document flow by interdependent persons in order to exclude funds from the taxable income of the individual engaged in making transit payments, including for the purpose of cashing out funds.

The practice of charging taxes on the entire turnover of transit companies as a way to combat cash-out may spread more widely, and may make their use an expensive and pointless pleasure.

What is a commodity loan?

Standard loans are usually taken out to purchase any goods or material assets. However, instead of money, the entrepreneur can immediately take these goods/things. In this case, there is an obligation to return them. Typically, an agreement on such loans is concluded between two legal entities.

Commodity loan agreement: what affects taxes and accounting for the borrower ?

The transfer of things, not money, is the main characteristic of commodity loans. Other nuances are determined by the specific agreement:

- The presence or absence of interest.

- The obligation to return the same asset or similar thing.

Commodity loans are a special form of lending. Drawing up an agreement on such a loan requires compliance with a number of rules.

How is the lender's accounting done when the borrower repays a commodity loan ?

Free loan as a way to hide payment for goods

Another category of cases related to the use of interest-free loans is the substitution of payments for goods with loans (Resolution of the Arbitration Court of the North Caucasus District dated October 28, 2019 in case No. A32-35646/2018; Resolution of the Arbitration Court of the North Caucasus District dated April 8. 2019 in case No. A53-34226/2017).

In some cases, taxpayers try to retain the right to use the simplified tax system in this way. When selling a product, “cunning” entrepreneurs do not receive payment for it, thereby reducing revenue. However, the trick quickly turns into stupidity when, instead of paying for the goods, the buyer receives a loan, and an interest-free one at that (even worse if the loan is equal to the cost of the goods delivered). The situation is not helped even by the fact that the loan is issued not by the buyer, but by another company (Decision of the Supreme Court of the Russian Federation dated April 3, 2019 in case No. A03-384/2018).

Obviously, in such a situation, it will not be difficult for the tax authority to prove that the sole purpose of such a loan was the taxpayer’s desire to retain the right to apply a special tax regime (Resolution of the Volga District Arbitration Court dated January 29, 2020 in case No. A12-9362/2018).

In other cases, replacing payment for goods with interest-free loans is used as a way to hide the fact of payment for goods in order to avoid paying VAT. Thus, in case No. A04-9919/2017, the tax authority indicated that transactions between the company and its related parties to provide loans without paying interest were used by the taxpayer in order to hide the actual sale of goods to related parties, to understate revenue and, accordingly, the taxable base for VAT, since the issuance of gratuitous loans is not typical for relationships that would take place between counterparties independent of each other, acting independently and on a strictly entrepreneurial basis (Decision of the Supreme Court of the Russian Federation dated April 12, 2019 in case No. A04-9919/2017).

Another special case is an interest-free loan as a way of concealing the fact of purchasing property from an interdependent person in order to avoid paying property taxes. In one of the cases, a situation was considered when, with the help of a loan, they tried to hide the purchase and sale of cars, for which, instead of payment, the buyer was issued a loan for the same amount (Decision of the Supreme Court of the Russian Federation dated May 27, 2019 in case No. A64-929/2017).

conclusions

Before lending money, you need to select a suitable document to protect your rights as a lender. If the amount is small, then you can limit yourself to a receipt. In all other cases, an agreement should be drawn up. This could be a loan agreement. It must indicate the details of each party. This is your full name, registration address, passport details and place of birth. It is also necessary to agree on the amount of debt and the timing of its repayment. If there is an interest rate, then it is indicated in the contract. You can also prescribe the conditions for reducing it in case of early repayment of the debt.

The agreement must be drawn up in writing, and in case of significant amounts, it must be certified by a notary. Concluding a transaction with a notary protects both parties from groundless claims in the future.

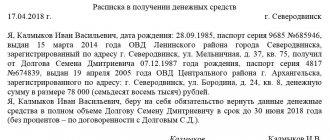

Important! The fact of transfer of money is recorded using a receipt.

After affixing your signature, you should write a full transcript of your full name on each document.

If the collateral amount exceeds one million, then a loan agreement must be drawn up. After signing, the documents are submitted to Rosreestr for registration and an encumbrance is placed on the pledged property. Accordingly, until the date of full repayment, the borrower cannot sell or give away property without the consent of the lender.

If the debtor fulfills the terms of the transaction in bad faith and allows delays, the lender has the right to apply to a notary for a writ of execution. After putting down the appropriate mark, you can contact the bailiffs, bypassing the court.

As for the pledge agreement, if the terms are violated, the creditor can file a claim in court. By decision of the court, the property will be put up for auction, and the funds received will be transferred to the lender to pay off the debt.

According to the recommendation of many notaries, any debt should be formalized in the form of an agreement and preferably notarized. The receipt also has legal force, but it will be quite difficult to get your money back, having only this in hand.

Errors when accounting for amounts under gratuitous loan agreements

There are many cases in which there was a simple mistake by the taxpayer, which led to non-payment of tax. There are many such errors when issuing interest-free loans to individuals by organizations that must withhold personal income tax as a tax agent on material benefits on interest for the use of borrowed funds (Resolution of the Arbitration Court of the Far Eastern District dated October 9, 2019 in case No. A04-3940/2018; Resolution of the Arbitration Court Volga District dated February 28, 2020 in case No. A65-10597/2019).

However, there are also isolated cases with exceptional errors, when it is not entirely clear whether the taxpayer made a mistake or whether he was counting on the inattention of the inspectors.

For example, in case No. A57-4930/2019, the courts came to the conclusion that it was unjustified for the company to reduce the income portion by the amount of returned advances, believing that the advance payments returned by the company are not a return under a supply agreement, but are a return of an interest-free loan under another agreement, which is confirmed letters with the counterparty, interrogation protocol, coincidence of the amounts returned under the supply agreement and under the loan agreement.

Simply put, the taxpayer formalized the return of funds under the loan agreement as a return of the advance payment under the supply agreement, reducing the amount of taxable income. The tax authority noticed the error.

Whether the taxpayer intended to avoid paying taxes, or whether a simple mistake was made, history is silent.

As another case of a tax accounting error, we can cite case No. A63-2828/2018, in which the taxpayer did not write off accounts payable under an interest-free loan agreement issued by a person that was liquidated at the time of the audit.

During the audit, the tax authority came to the conclusion that in this case the taxpayer has non-operating income on which it is necessary to pay income tax.

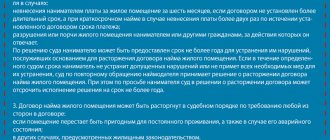

Conditions for changing and early termination of the loan agreement

If you need to terminate an interest-free loan agreement between individuals earlier, this can be done in the same way as an interest-bearing agreement. All the subtleties of this process are spelled out in Articles 450 and 452 of the Civil Code of the Russian Federation, where there are conditions not only for terminating, but also for changing the contract.

If changes are made to the document, they must be specified in an additional agreement. It is attached to the main contract and becomes an integral part of it.

In case of any concerns, the parties can individually stipulate early termination of the contract, and under what conditions it can occur. Typically, such a measure is introduced only by agreement of the parties. If there is no such agreement, the contract can be terminated early solely for the reasons specified in Article 450 of the Civil Code of the Russian Federation.