Last update: 04/28/2021

Question:

What is the distribution of property tax deductions between spouses when purchasing an apartment? Why is this needed, and how is it done?

Answer:

As you know, when purchasing a home, our state provides a pleasant benefit to each Buyer in the form of a property tax deduction (Article 220 of the Tax Code of the Russian Federation). This also applies to spouses who purchase an apartment as common property.

What is the essence of the deduction? The state is ready to return to the Buyer 13% income tax on the purchase amount up to 2 million rubles. And also - return 13% of the mortgage interest paid up to 3 million rubles.

In total, the total amount that is returned to the Home Buyer can reach = (2,000,000 rubles x 13%) + (3,000,000 rubles x 13%) = 260,000 + 390,000 = 650,000 rubles. (maximum) .

And such a tax refund is due to each spouse when purchasing an apartment!

Why then distribute the deduction between husband and wife ? For what purpose? For optimization purposes! That is, in order for the maximum possible amount to be returned to the family from both spouses, and for this amount to be returned as quickly as possible. That's it in a nutshell.

To understand this issue in more detail, you need to understand the following points:

- Can both spouses receive a full for the purchase of one apartment?

- How does the form of ownership the tax refund?

- How are mortgage payments when returning personal income tax to each spouse?

- What is the distribution of tax deductions between spouses for the joint purchase of an apartment, and how does it happen?

- How should the size of shares be established for each spouse when distributing deductions between them (including for mortgage interest)?

A little patience - now we will clarify everything and give examples.

Help in filing a tax return and obtaining a tax deduction can be obtained HERE (SERVICES).

13% personal income tax refund when spouses purchase an apartment

IMPORTANT! The rules described below apply to those apartments that were purchased after January 1, 2014 (what happened before this date can be read here).

Let's start with the fact that the acquisition of living space itself can be formalized by spouses in three ways:

- into common joint ownership;

- into common shared ownership;

- in the property of one of the spouses; at the same time, the second spouse still becomes a co-owner of the property, according to the law on joint property of spouses.

You can read more about these types of property by following the links in the Glossary. Here we will show how the property deduction (personal income tax refund) in such a joint purchase of an apartment by spouses, including with the use of a mortgage.

And we’ll also tell you how you can get a deduction for children .

The basic rules for accepting a new apartment from the Developer - see the Glossary at the link.

Distribution of tax deductions between spouses - what is it and how to apply?

Distributing the tax deduction for the purchase of an apartment between spouses allows you to reduce the amount of deduction for one of them, and thereby increase the amount of the other. That is, one spouse refuses the tax refund due to him (or part of it) in favor of the other spouse, helping him return a larger amount, within the maximum limits - 2 million rubles. per person (deduction for purchase), and 3 million rubles. per person (mortgage interest deduction).

At the same time, the distribution of the personal income tax refund between spouses for the main deduction (for the purchase of housing) does not depend on the distribution of the tax refund for the mortgage interest paid. That is, these two types of deductions are not related to each other and can be distributed in different proportions.

IMPORTANT to understand! The distribution of the property deduction does NOT mean that one of the spouses can receive a double deduction for both (for themselves and for the spouse). The right to deduction itself is not transferred to anyone! The spouses only redistribute their stated (declared) expenses for the purchase of an apartment . And in accordance with these amounts, they receive deductions limited to the above limits.

In other words, the logic of the law is such that it allows the return of 13% of the amount that each spouse spent on the purchase of housing (literally, “a deduction in the amount of expenses actually incurred”). This applies to both the cost of purchasing an apartment and the cost of paying interest on a mortgage.

How will the state know which spouse invested how much in the purchase of a common family nest?

Tax authorities here rely on one of the following facts:

- availability of payment documents (if each spouse documents his personal investments in common property);

- form of ownership of real estate (with shared ownership, it is assumed that the spouses incurred expenses in accordance with the size of their shares, and with joint ownership, the shares of the spouses are assumed to be equal);

- a statement from the spouses on the distribution of their expenses for the purchase of an apartment (the husband and wife can arbitrarily distribute “actual expenses” among themselves, and it is for these amounts that each of them will be provided with a tax deduction).

If there is such a statement from the spouses regarding distribution , then the remaining facts (shares of property, etc.) are no longer taken into account.

Apartment purchase and sale transaction. For the list of documents for registration with Rosreestr , see the Glossary at the link.

In what cases do spouses decide to redistribute tax deductions among themselves? The reasons for this may be different, for example:

- One of the spouses does not have an official income, and accordingly, does not have the opportunity to use their right to a personal income tax refund. Then he transfers his right (more precisely, his share of the “actual expenses” for the total purchase) to the other spouse so that he can realize his deduction to the maximum.

- One of the spouses has a small income, and accordingly, pays a small personal income tax on it, which will take a very long time to return. Another spouse with a high income, when redistributing the deduction, will be able to return the money to the family faster.

- One spouse is due to retire soon (see tax credit for retirees). Then it is better to redistribute a larger share of the deduction to the spouse who continues to work.

- One of the spouses plans to use their right to a tax deduction when purchasing another home (when building a house, for example).

In such cases, the distribution of the property tax deduction by agreement between the spouses allows the maximum possible amount of the funds spent on the purchase of an apartment to be returned to the family (see examples below).

How to buy a mortgaged apartment that is pledged to the bank? 3 ways - see the link.

What amount of deduction (share of joint costs) will fall on the husband and wife during distribution - the spouses decide for themselves, regardless of their shares of property. An agreement on this is drawn up in the form of a joint application for the distribution of deductions (see below for a link to a sample), and is submitted to your territorial Federal Tax Service at your place of residence.

Moreover, the spouse who, as a result of such redistribution , refused his part of the tax deduction when purchasing one apartment (they say, he did not personally participate in these costs) does not lose his right to a tax refund. And he can use it in the future, when buying another home.

The application for distribution of property deductions is signed by both spouses. This application must be submitted along with the 3-NDFL declaration.

True, if the cost of housing is equal to or exceeds 4 million rubles. (and the apartment is registered in the name of both spouses), then redistributing the deduction between them loses its meaning . Why? Because in this case, each spouse already receives their maximum possible deduction (2 million rubles). And any redistribution will only reduce the share of one of the spouses, and will not increase the share of the second.

The exception is the only case when the apartment was NOT purchased in equal shares, and the share of “actual expenses” of one of the spouses is less than 2 million rubles. Then redistributing the deduction into equal shares between spouses will allow them to return the maximum possible amount to the family (260,000 rubles x 2 = 520,000 rubles).

A sample application for the distribution of property tax deductions between spouses for the purchase of an apartment can be downloaded HERE (SERVICES).

Expenses taken into account in the deduction

A residential property (or part of it) can be purchased ready-made or unfinished, built through equity participation in construction or on its own. For deduction, it is legitimate to take into account all costs directly related to its occurrence. In addition to the funds directly paid for the acquisition of an object or a share in construction, the following expenses can be taken into account:

- for design and budgeting;

- construction and completion;

- finishing (materials and work);

- connection to general networks or construction of local sources of water, gas, heat, electricity, as well as autonomous sewerage.

Costs for completion and finishing are taken into account only if the property was purchased unfinished or the contract provides for the transfer of housing to the owner without finishing (subclause 5, clause 3, article 220 of the Tax Code of the Russian Federation).

Distribution of tax deduction for mortgage interest between spouses

According to Article 34 of the RF IC, all property (including money) acquired during marriage is the joint property of the spouses. Accordingly, all expenses incurred by the spouses during the marriage are also considered common. This means that the cost of paying interest on a mortgage loan is also common, regardless of which spouse has a loan agreement. What follows from this?

From this it follows that even if one of the spouses does not appear in the loan agreement (for example, as a co-borrower or guarantor), he still has the right to receive a tax deduction for mortgage interest .

Spouses write a separate application for the distribution of property deductions for credit interest, and themselves determine the size of the shares of their “actually incurred expenses” for their payment. In accordance with these shares, each spouse will have access to a deduction in the amount of the specified expenses, but not more than 3 million rubles. (refundable RUB 390,000) per person. At the same time, it does not matter to whom the payment documents for loan repayment will be issued.

the tax deduction for interest paid on the mortgage among themselves, regardless of the distribution of the main deduction for the purchase of an apartment. That is, the proportions of these two deductions may not coincide.

In addition, spouses can redistribute the interest deduction in a different proportion . This is useful in the case when the ratio of current incomes of the husband and wife changes over time (for example, the wife went on maternity leave, or the husband quit his job).

A sample application for the distribution of tax deductions between spouses for mortgage interest can be downloaded HERE (SERVICES).

Now let’s look at EXAMPLES of spouses receiving a property deduction for different forms of ownership of an apartment.

Distribution of tax deductions for joint property of spouses

If an apartment is purchased as a joint property of both spouses, then their shares of ownership are assumed equal by default - that is, 50/50. And the tax authorities assume that the spouses also borne the “actual expenses” for the purchase of the apartment in this proportion.

But spouses have the right to redistribute their “actual expenses” among themselves in any proportion (up to 100% and 0%), indicating this in a tax application. And then each of them will receive a deduction in accordance with the amounts specified in the application, but not more than the established limits for each.

♦ Example-1 (Distribution of deduction for joint ownership ♦

Which Apartment Buyer is considered bona fide? And what does this mean in the event of a legal dispute? See the Glossary at the link.

Distribution of tax deductions for shared property of spouses

If the apartment is registered as common shared ownership (after January 2014), then a property deduction is also provided to each of the spouses in the amount of expenses incurred . By default, “expenses incurred” mean the property shares converted into rubles from the Apartment Purchase and Sale Agreement or the Equity Participation Agreement.

But even here, spouses can redistribute the tax deduction among themselves in any proportion. The main thing is that the amount of deduction per person does not exceed the established limit of 2 million rubles. (The Federal Tax Service confirms this here).

♦ Example-2 (Distribution of deductions for shared ownership ♦

Is it possible to return personal income tax for the purchase of an apartment if it has already been sold - see the answer at the link.

Distribution of tax deductions when registering an apartment for one of the spouses

If the purchased apartment is registered solely in the name of only one of the spouses , then according to the law (Article 34 of the RF IC), in the absence of a marriage contract, the real estate is still their common property . Therefore, the tax deduction can be distributed between the spouses even in this case.

The situation here is similar to that if the apartment was registered as a common joint property (see above). The spouses set the “actual costs” for purchasing an apartment themselves, and receive a personal income tax refund in accordance with the expenses specified in the application (within established limits).

♦ Example-3 (Distribution of deductions when applying for one spouse ♦

In general, if the cost of an apartment purchased and registered in the name of one of the spouses is equal to or more than 4 million rubles, then there is always a reason to apply for the distribution of the tax deduction between the spouses in a 50/50 ratio. This way, the maximum possible amount will be returned to the family (260,000 x 2 = 520,000 rubles).

And even if one of the spouses at this moment does not have the opportunity to use the right to a deduction (he quit his job, for example), he will apply it in the future to the same apartment (when he returns to work).

fill out the 3-NDFL declaration and complete all the documents to receive the deduction on their own. But it takes time and effort. And this does not always work out the first time (due to errors in filling out documents, they are not accepted). It is much easier and faster to entrust this matter to tax consultants.

Consultation and assistance in filing a 3-NDFL declaration and obtaining a tax deduction can be obtained HERE (SERVICES).

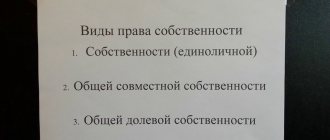

Difference between joint and shared ownership

- With shared ownership, a property is owned simultaneously by several individuals.

It is divided into shares (not necessarily equal). The owners can be both relatives and people not related by blood. Important! Shares must be clearly demarcated and confirmed by official documents - certificates of ownership. - Joint property is property that is owned simultaneously by two persons.

It is not divided into shares. This form of ownership arises among spouses after official marriage. This is especially true for property acquired after registration of the relationship. It doesn’t matter who contributed how much money. Now they can sell it only with mutual consent. The opposite situation is that the couple lives together, but the relationship is not registered. They make a joint purchase, paying for it in half. But in this case, the property will not become joint.