The legislative framework

The key regulatory act in the field of bankruptcy is Federal Law dated October 26, 2002 No. 127-FZ “On Insolvency (Bankruptcy)”. In 2015, amendments were made to it, giving the opportunity to become bankrupt not only for a legal entity, but also for an individual (Chapter X). Law on Bankruptcy of Individuals 127-FZ (Part 1, Article 2):

- establishes the grounds for declaring the debtor bankrupt;

- determines measures to prevent bankruptcy;

- regulates the procedure and conditions for conducting bankruptcy proceedings;

- regulates other relations that arise when a debtor is unable to pay off debts.

Lawsuits and decisions

If you are under legal proceedings for debt collection, or if there are already court decisions, list them. After the introduction of the sale of property and during restructuring, financial claims must be considered by the Arbitration Court, which conducts the bankruptcy case.

Enforcement proceedings are suspended and settlements take place within the framework of the Insolvency Law. But alimony payments and compensation for harm to life and health do not stop - the financial manager will pay money to such claimants from your income.

Margarita Kholostova

financial manager

In this section, also include information about writing off money from your accounts if banks or bailiffs have already partially collected money from you.

Grounds for bankruptcy

To initiate a bankruptcy procedure, it is necessary that the bankruptcy conditions for individuals be met. Only if they are observed can the debtor file bankruptcy for an individual, for example, for loans

Signs of bankruptcy:

- the amount of debt is at least 500 thousand rubles and the debtor’s obligations are overdue for at least 3 months, in this case a trial is held in an arbitration court (Part 2 of Article 213.3 127-FZ). The debtor himself, the bankruptcy creditor or the authorized body has the right to file for bankruptcy independently (Part 1 of Article 213.3 127-FZ);

- the amount of debt is from 50 thousand to 500 thousand rubles, in this case the debtor can be declared bankrupt under a simplified procedure, that is, out of court upon application (Part 1 of Article 223.2 127-FZ).

Date, signature

Place a date and signature at the end of the application.

note

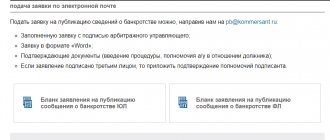

, before filing with the court, you must send all creditors copies of the application and documents (only those that they do not have), by registered mail with return receipt requested. Postal receipts must be included in the application package (item 7 in our list), otherwise the application will be left without progress until the postal receipts are received.

After completing the collection of papers and writing the application, you can file an application for bankruptcy of an individual in court.

Bankruptcy of individuals is not just a formal procedure. If the position is not clearly stated or there is insufficient evidence, the court will refuse or leave the case without consideration.

To avoid such troubles, be careful!

Features of the simplified procedure

Extrajudicial bankruptcy is regulated by the provisions of §5 127-FZ. It allows, if the conditions set out in the previous section are met, to file bankruptcy for an individual free of charge. Here are excerpts from articles §5 127-FZ, illustrating the features of simplified bankruptcy of individuals through the MFC:

- Enforcement proceedings have been completed against the debtor due to the lack of property on which collection can be imposed, the enforcement document has been returned to the claimant (Part 1 of Article 223.2);

- the debtor files an application for declaring him bankrupt through the MFC at his place of residence (Part 2 of Article 223.2);

- the debtor attaches to the application a list of all creditors known to him and their claims (part 4 of article 223.2);

- During the day, the MFC checks the fact of the return of the writ of execution to the claimant and, upon confirmation, makes an entry about the initiation of extrajudicial bankruptcy proceedings in the federal register, otherwise the application is returned to the debtor (Part 5 of Article 223.2);

- from the day the information is included in the federal register, a moratorium is introduced on satisfying the claims of creditors (Part 1 of Article 223.4);

- if during the procedure the debtor acquires any property (for example, accepts a gift, enters into an inheritance) that allows him to fully or partially repay debts, he must notify the MFC about this within 5 days (Part 1 of Article 223.5);

- after receiving such a notification, the MFC, within 3 days, enters into the federal register information about the termination of the extrajudicial bankruptcy procedure;

- after 6 months from the date of inclusion of information about the initiation of extrajudicial bankruptcy proceedings in the federal register, the procedure is completed, and the debtor is released from further fulfillment of the claims of the creditors indicated in the application (Part 1 of Article 223.6).

Stage IV. Procedures applied in a bankruptcy case

Website of the authors of the article : https://moe-bankruptcy.rf/

(1) Restructuring of a citizen’s debts

Restructuring involves restoring the solvency of an individual by changing the terms of payment of debt to creditors.

In order for a debt restructuring procedure to be applied to an individual, he must meet the following requirements:

- receive a stable income so that, in addition to paying off debts, you can satisfy your basic needs,

- not be convicted of economic crimes,

- not be prosecuted for administrative offenses related to theft or destruction of property, deliberate bankruptcy,

- have not made bankruptcy decisions within the last 5 years,

- do not have a debt restructuring plan for the last 8 years.

The debt restructuring plan forms the basis for the implementation of the procedure. It can be offered either by the debtor himself or by the creditor or an authorized body. The draft plan is sent to the financial manager within 10 days after the register of creditors' claims is compiled. If no one proposes a project, then at a meeting of creditors the issue of declaring the citizen bankrupt and selling his property will be decided.

The plan approved by the meeting of creditors is subject to court approval. After which it must be completed within 3 years.

The approval of a debt restructuring plan leads to the following:

- creditors cannot make claims outside the terms of the plan and demand compensation for losses associated with its approval,

- the debt cannot be repaid by offsetting a counterclaim,

- interest, penalties and fines for the requirements stated in the plan will not be accrued,

- the debtor is obliged to notify creditors if his property situation changes significantly,

- during the implementation of the plan and for 5 years after its completion, the citizen must not hide the fact that the restructuring procedure has been applied to him.

When a debt restructuring plan has not been presented, not approved by a meeting of creditors, or canceled by the court, then a decision is made against the debtor to declare him bankrupt and introduce a procedure for the sale of property.

(2) Sale of a citizen’s property (bankruptcy estate)

If restructuring is impossible, the result of bankruptcy is the sale of the citizen’s property at auction and payment to all creditors in proportion to the debt (taking into account priority).

After the court makes a decision to apply this procedure to the debtor, the financial manager within 15 days notifies the creditors and invites them to submit their claims.

The bankruptcy estate includes all property that may be subject to foreclosure, wages and other sources of income. If the debtor owns the property jointly with other persons (for example, a spouse), only his share is subject to seizure.

The inventory and assessment of the property is carried out by the financial manager, who then submits regulations on the procedure, conditions and timing of the procedure to the court. It also reflects the initial sale price of the property.

The following are exempt from collection:

- residential premises, if it is the only dwelling,

- a plot of land where the only housing is located,

- household items, with the exception of jewelry and luxury items,

- child support for minor children,

- pension and benefits,

- money in the amount of the subsistence minimum, etc.

The sale of the bankruptcy estate is carried out through auctions. They are given 2 months to complete. After which the debt is repaid.

The order of satisfaction of creditors' claims is established by Article 213.27 of Federal Law No. 127-FZ.

The first priority includes current payments, including those related to the conduct of a bankruptcy case. This includes 7 percent, which the financial manager receives as remuneration in addition to a fixed payment of 25 thousand rubles (the price of bankruptcy of an individual depends on the size of satisfied creditors’ claims.

If the proceeds are not enough, the bankrupt is released from his obligations to cover debts to creditors. But the law also specifies cases when writing off debts of individuals (for loans, loans, taxes, etc.) is unacceptable:

- The citizen was held accountable for unlawful actions during bankruptcy, including fictitious bankruptcy.

- Avoided providing required information or provided false information.

- During the fulfillment of obligations, illegal actions were committed, for example, fraud or intentional destruction of property.

The sale of a citizen's property is carried out no more than 6 months in advance.

(3) Conclusion of a settlement agreement

The settlement agreement stops the actions of the bankruptcy trustee, the citizen begins to repay the debt, and the proceedings are terminated.

The settlement agreement applies to the claims of creditors included in the register. If disagreements arise between the participants in the process, the terms of execution of the agreement are considered by the court.

If the terms of the settlement agreement are violated, then bankruptcy proceedings are resumed and a procedure for the sale of property is introduced against the debtor.

[to contents