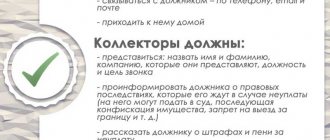

Debt collection under a writ of execution is a long, complex and unpleasant procedure for both parties: the debtor and the creditor. Nevertheless, there are situations when such a step cannot be avoided. The procedure provides for two ways to repay debt in open proceedings: voluntary and forced.

If in the first case, with independent collection, the process can be completed quite quickly, then the involvement of bailiffs, as a rule, significantly extends the return of money over time. Read our material about how to initiate the debt collection procedure under a writ of execution, how to behave if you are a debtor, and how to better control the work of the BSC.

Collecting evidence of debt

Without evidence of the existence of a debt (loan agreement), collection of debts from individuals is impossible, unless the debtor pays off voluntarily.

What can be evidence of debt :

- loan agreement (or other agreement under which the debt arose;

- receipt.

A correctly executed loan agreement or receipt will be indisputable evidence for the court. These documents must contain the loan amount, terms and procedure for repayment, confirmation of receipt of cash by the borrower.

If the agreement was concluded remotely over the Internet by signing documents by entering codes received by the borrower on the phone, such an agreement also has legal force.

In addition, if there is no agreement, as evidence the court accepts witness testimony, primary documents and payment documents, as well as correspondence by e-mail, SMS, messaging in instant messengers and social networks, certified by a notary, video and audio recordings.

Payment methods for services

You can pay for our services in the following ways:

- Cash in the office.

- By bank card.

- By bank transfer according to the bureau details.

The calculation of the cost of services is transparent so that you understand what you are paying for. We have several packages with one-time and subscription fees that allow customers to save money.

Leave a request on the website or call to schedule a free consultation with a lawyer, and we will provide comprehensive assistance in debt collection with minimal losses for you!

We calculate the total amount we will demand

For late repayment of debt, an individual can be demanded not only the amount of the principal debt, but also all the penalties specified in the agreement (receipt). It can be:

- interest on the use of borrowed funds;

- interest for late repayment of debt;

- a fine in a fixed amount;

- losses (lost profits).

If penalties are not specified in the contract, then you can collect “legal” interest on the amount of debt under Art. 809 of the Civil Code of the Russian Federation and for the use of other people's funds under Art. 395 of the Civil Code of the Russian Federation, which are calculated at the key rate of the Central Bank of the Russian Federation.

We will help you correctly calculate how much to demand from the debtor.

If you have to file a lawsuit in court, you can additionally demand reimbursement of all court costs, including state fees, delivery of witnesses, and costs for a lawyer.

Stages of working with accounts receivable

When you realize that a problem receivable has formed, you collect and analyze information.

Find out the reasons why the counterparty cannot or does not want to return the money in accordance with the contract. The next step is a reminder. You methodically remind the debtor about the debt. The more often you do this, the more often the debtor remembers the debt.

Information is needed to create a positive-negative context. A positive context is the client’s desire to continue cooperation. Negative - your cooperation is hampered by the resulting debt. You do not threaten, but calmly inform the debtor of your desire to receive money. To understand the difference between threatening and informing, compare the two expressions. The later you pay, the worse - threat. The sooner you pay, the better - information.

You have created an information space, prepared the debtor for the necessary decision, and now enter negotiations from a strong position. In negotiations, you clearly identify the problem and demand that it be resolved.

You invite an agent to make him a “bad cop.” You don't want to spoil your relationship with the debtor, so assign the role of the villain to the agent. The agent uses the entire negotiating arsenal: pressure, threats and even blackmail.

If negotiations and the agent's assistance do not bring results, the court remains. Litigation is a sign of weakness. You were unable to collect the debt yourself and are now looking for an intercessor in the person of the state.

The last stage is forced collection. It takes place according to one of three scenarios: • Enforcement proceedings are a tool for protecting the borrower. • Bankruptcy is a tool for protecting the debtor. He doesn't owe you anything because he has nothing to pay. • Criminal prosecution. Here the state pursues not your interests or the interests of the debtor, but its own - to punish the culprit.

Statistics on the work of bailiffs from 2007 to 2021

Statistics clearly show that you should not rely on bailiffs. Not only is the percentage of collections low, but collection can also drag on for years.

Factors influencing debt repayment 33% chance of repayment if you break the debt into parts. 30% if you give the opportunity to defer payment 25% forced collection procedure 9% to repay the debt under the agreement, without additional activities 4% the presence of a judicial act. The problem is that the court requires immediate repayment, but the debtor, as a rule, does not have such an opportunity. 3% debt on receipt

Let's calculate the effectiveness of pre-trial collection methods: term 30% + debt amount 33% + debt under contract 9% + debt under receipt 3% = 75%

The judicial act and the collection procedure give us only 29%.

Conclusion: at the moment, pre-trial methods of collection are more effective than judicial ones.

We agree without court

Contact the debtor and agree on an installment plan, postponing payment for a certain period, after which you intend to file a lawsuit and contact law enforcement agencies.

For example, if the amount of debt is more than 2.5 million rubles and it is known that the debtor has money in his accounts and valuable property, including luxury items, but he deliberately evades repayment of the debt, then such behavior falls under the signs of malicious evasion of debt repayment (Article 171 of the Criminal Code of the Russian Federation).

What to do if proceedings are initiated

Litigation often frightens people. If they find out that they have received a letter about the start of the process, a common first reaction is panic. But hasty actions will not change the situation and will not help matters. The best option is to calm down and try to find solutions. As a rule, you can come to an agreement with the creditor: running away is not the best tactic, since the debt will not go away. EOS prefers to offer clients a variety of options for solving the problem rather than going to court. If we are talking about a bank, try not to worry and try to contact representatives of the lender to clarify the situation. Active participation in the process and willingness to pay obligations will play into your hands even in difficult circumstances.

We send a pre-trial claim

A pre-trial claim indicates the seriousness of your intention to go to court, and may encourage you to repay the debt (or part of the debt). We provide a written justification for the requirements with references to the provisions of the law, calculation of the debt with interest and fines. We attach evidence to the claim.

Important! Warn the debtor that if you go to court, in addition to the principal debt, interest and fines, you will be charged a state fee, all court costs and legal expenses.

It is not necessary by law to send a pre-trial claim to a debtor-individual, with the exception of 2 cases:

- when a provision for pre-trial procedure is in the agreement (receipt);

- if the agreement (receipt) does not indicate the exact loan repayment period.

If you have written a pre-trial claim, you need to wait 30 days for a response or translation, and then file a claim (Article 810 of the Civil Code of the Russian Federation). Has the debtor failed to comply within 30 days? You can go to court.

Types of accounts receivable

In practice, debt can be divided into categories.

By duration:

- for short-term (when payment is due within a year after the due date of the report);

- and long-term (when payment is expected a year after the reporting date).

According to the repayment prospect

- to normal;

- and expired (doubtful and hopeless).

Normal

It occurs when one party has already fulfilled the contract (property delivered; services rendered), but the payment date is still ahead.

Overdue

Occurs when the due date has arrived and the payment has not been made.

Doubtful and bad debts

The concept of doubtful and bad debts is given in the Tax Code of the Russian Federation (Article 266). The main difference is the possibility of repayment. In the first case, the possibility of collecting the debt is not lost; in the second, such a possibility is excluded.

Signs of doubtful debt: execution of the transaction by the counterparty has been received; the payment deadline has already passed; there is no security for the debt with a pledge, surety or bank guarantee.

in a doubtful until the time limit for filing a claim has expired.

After this period, the debt goes into the category of hopeless (unrealistic) for collection.

The debt is taken into account as unreal when there are any of the signs established by paragraph 2 of Art. 266 Tax Code of the Russian Federation:

- The claim period has expired.

- The debtor's obligation is terminated due to the impossibility of fulfilling it (confirmed by an act of a state body) or liquidation. This includes cases where the debtor has ceased to operate as a legal entity.

- The bailiff ruled that it was impossible to collect the debt (it was not established where the debtor was located, there was no information about his property and money).

- The citizen is declared bankrupt and released from fulfilling the claims of creditors.

Most often, a bad debt is formed when the debtor company is liquidated or when the statute of limitations expires.

| Normal | It occurs when one party has already fulfilled the contract (property delivered; services rendered), but the payment date is still ahead. | ||

| Overdue | Doubtful | Signs | Term |

| The payment date has arrived, but the payment has not been made. The possibility of collecting the debt is not lost. Execution of the transaction by the counterparty has been received; There is no security for the debt with a pledge, surety or bank guarantee. | Before the expiration of the period for filing a claim | ||

| Hopeless | From doubtful debt to bad debt. There is no possibility of collection. Causes:

| The claim period has expired. | |

Let's go to court

We apply to the court of general jurisdiction according to the registration or place of residence of the debtor. Cases with the value of the claim (debt of an individual) of no more than 50,000 rubles (for property disputes arising in the field of consumer rights protection, no more than 100,000 rubles) and applications for the issuance of a court order with the amount of claims not exceeding 500,000 rubles are considered by the world court court. In all other cases, we turn to the city (district) court.

The address of the required court can be found on the website of the State Automated System of the Russian Federation “Justice”.

We write a statement of claim according to the provisions of Art. 131 of the Civil Code of the Russian Federation (we will help you draw it up correctly).

You can file a claim in person at the court office, by mail or through the Internet services “My Arbitr” and GAS “Justice”.

Important! We recommend filing an application for a court order; this is the fastest way to “justice” the debt. The debtor will only have 10 days to cancel the order.

Debt collection through the court is also possible in bankruptcy proceedings if the total debt of a citizen is more than 500,000 rubles.

How to protect a company from debtors

An effective way to avoid cooperation with a potential debtor is to check your credit history. This document will show how the company or individual entrepreneur handled borrowed money and how regularly they repaid debts. Credit history will show past and present delinquencies. Current arrears are the most obvious stopping factor. If the counterparty does not pay the bank, then it certainly will not pay you.

Get a credit report

The article was prepared based on the presentation of Alexander Vladimirovich Matveev, president of the NP “Society for the Protection of the Rights of Creditors and Claimants.” Website: www.enabling.ru

We contact banks and the FSSP with a writ of execution

After the court decision comes into force (30 days after the preparation of a reasoned decision), you can obtain a writ of execution and present it to the banks where the debtor has accounts. As money is received, it will be written off in your favor (up to 50% of amounts, for example, wages and other income).

If the debtor is not officially working and there is no money in the accounts for 1 - 2 months, contact the FSSP. Take part in collection, look for information about accounts and property, help bailiffs with the delivery/sending of documents, letters, etc.

Situation analysis for free

By contacting our office for help in debt collection, you can count on a comprehensive analysis of the situation.

Already at the first meeting, lawyers will select the necessary data to effectively resolve the issue and develop an optimal plan. Before your consultation, be prepared to provide us with more information and ask any questions you may have.

Karbanov Petr Petrovich

To get a consultation

We use “new” methods of debt collection from individuals

Courts are increasingly accepting “technological” evidence: correspondence, photos and videos on social networks, screenshots. So, in one case of debt collection in bankruptcy, a girl published photos on social networks with a car that she officially sold shortly before she took on the debt. The financial manager saw on VKontakte that after the sale of the car, the debtor continued to use the foreign car, confirmed this with screenshots and challenged the transaction.

This example of a debt collection case shows how modern technology has expanded the ability to obtain evidence. It is enough to show persistence and ingenuity.