Author of the article: Yulia Kaysina Last modified: January 2021 13970

Dividends - profits paid to the founders, co-founders and shareholders of the organization - are considered income from which alimony is deducted. However, this type of profit is very specific, so alimony from dividends can be difficult to calculate. There is no separate article concerning them in the Family Code. Therefore, in judicial practice and accounting calculations, they are guided by general provisions, taking into account the characteristics of this type of profit.

What are dividends

Dividends are part of the net profit that is distributed among participants and shareholders. The following are recognized as dividends (clause 1 of Article of the Tax Code of the Russian Federation):

- any income distributed in proportion to the contributions of participants or shareholders and paid from the net profit of the organization;

- income from sources abroad, if they are recognized as dividends under the laws of a foreign state;

- the difference between the income received upon leaving the organization or upon its liquidation, and: for income tax - the actually paid cost of shares, interests or shares, taking into account cash contributions to the property;

- for personal income tax - expenses for the acquisition of shares, shares, shares.

Payments that do not relate to dividends are listed in clause 2 of Art. Tax Code of the Russian Federation.

Organizations that pay dividends to foreign participants should first look at the double tax treaty (if there is one). The concept of dividends in it may differ from the Tax Code of the Russian Federation. For example, under some agreements, dividends may not be distributed in proportion to contributions.

On May 12, an online course for advanced training “Income Tax. Complex issues in accounting and tax accounting, practical recommendations"

Take a course and receive a certificate of advanced training

How to pay dividends

To pay dividends, you need to make an appropriate decision, determine the amount and sources for payment, and also make sure that the organization has the right to distribute profits. The rules are different for LLCs and JSCs. We have collected them in the table:

| Parameter | OOO | JSC |

| Payment decision | Accepts the general meeting of participants or the only participant | Hosts the general meeting of shareholders |

| Frequency of payments | Based on the results of the year or intermediate periods (quarter, half-year, 9 months) | Based on the results of the year or interim periods (quarter, half-year, 9 months) Restriction: the decision on payment is made no later than three months after the end of the interim period |

| Dividend amount | Proportional to the participants’ contributions to the authorized capital, but only when the charter does not provide otherwise | In the amount declared for shares of each category |

| Payment source | Net profit | Net profit |

| Deadline for payment | 60 days after the distribution decision | 25 working days from the date on which persons entitled to receive dividends are determined |

| Prohibition on payment of dividends |

|

|

What to do if interim dividends turned out to be more than net profit for the year, answered the experts at Kontur.School.

Combined option

If the father or mother works, for example, as a director of an LLC and receives dividends from its activities, then the court may well settle on a combined accrual option. In particular, a certain percentage will be withheld from the salary in accordance with current legislation. Plus, based on the fact that the payer has another source of income (dividends), the court may oblige him to transfer an additional specific fixed amount in excess of the share.

This solution protects the interests of the child well, since the total amount of payments is usually sufficient to meet his needs. In addition, as part of this decision, you can calculate in advance exactly how much will be allocated for the baby.

However, the option under discussion has its pitfalls: if the total amount turns out to be too large, the defendant in court may pay attention to this and declare that he is ready to fulfill his obligations to support the child, and not contribute to the unjust enrichment of the second parent living with him. Given this, there is a possibility that the fixed amount will be quite small.

This kind of work ahead of the defendants' arguments has helped us repeatedly win cases and achieve fairly large amounts of alimony for our clients. However, keep in mind that preparation is key here. And it takes time. Therefore, do not delay your application.

How to record dividends in accounting

The payment of dividends based on the company's performance for the reporting year is an event after the reporting date. It is disclosed in the explanatory note. Accounting entries will be made already in the payment period.

For dividends to individuals, the postings are as follows:

- Dt 84 Kt 70 (75) - dividends accrued;

- Dt 70 (75) Kt 68 - personal income tax is withheld upon payment;

- Dt 70 (75) Kt 51 - dividends paid;

- Dt 68 Kt 51 - transferred to the personal income tax budget.

For dividends to legal entities:

- Dt 84 Kt 75.02 - dividends accrued;

- Dt 75.02 Kt 68 - income tax is withheld upon payment;

- Dt 75.02 Kt 51 - dividends paid;

- Dt 68 Kt 51 - income tax is transferred to the budget.

You will need supporting documents: minutes of the general meeting of shareholders (participants) and an accounting certificate. We recommend that you do not neglect documents. Regulatory authorities pay a lot of attention to dividends. After almost every payment, the tax office sends a request: to whom it was paid and how, where the tax was withheld, when it was paid and asks to present an accounting certificate and the decision of the general meeting.

Calculate dividends and withholding tax taking into account current requirements

Try for free

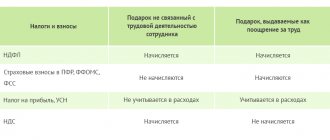

How are dividend payments taxed?

Dividends paid by a JSC or LLC are not recognized as expenses for the purposes of calculating income tax. They are paid from net profit and are included in Art. 270 of the Tax Code of the Russian Federation, which lists expenses not taken into account for income tax.

The organization withholds personal income tax or income tax when paying dividends. Personal income tax - on dividends to individuals, income tax - on dividends to legal entities. But there are two exceptions: payment by a Russian organization through a depository and payment by a foreign organization. There is no need to pay insurance premiums in any case.

Tax on dividends to a legal entity

Income tax rates on dividends are presented in the table:

| Type of dividends | Bid | Base |

| Received by Russian organizations from Russian and foreign organizations | 13% - in standard cases; 0% - if the share of the deposit is 50% or more, and the continuous holding period is at least 365 days | clause 3 art. 284 Tax Code of the Russian Federation |

| Received by legal entities non-residents of the Russian Federation | 15%, unless another rate is established by a double tax treaty | clause 3 art. 284 Tax Code of the Russian Federation |

Income tax on dividends to Russian resident organizations is calculated according to the formula (clause 5 of Article 275 of the Tax Code of the Russian Federation):

N = K × CH × (D1 - D2), where:

- N - amount of tax to be withheld;

- K is the ratio of the amount of dividends subject to distribution in favor of the recipient of dividends to the total amount of distributed dividends;

- Сн - tax rate;

- D1 - the total amount of dividends to be distributed in favor of all recipients;

- D2 - the total amount of dividends received from other organizations (what has changed in 2021?).

If the amount of dividends received, taxed at a rate of 13%, is greater than the amount of dividends paid (D1 < D2), then the withholding tax (N) will be negative. Then it is not calculated and is not reimbursed from the budget.

When dividends are paid to foreign legal entities non-residents of the Russian Federation, a rate of 15% or another established by international agreement is applied. The formula is simple (clause 6 of Article 275 of the Tax Code of the Russian Federation): N = Cn × D.

Dividends to foreign companies and non-resident individuals are taxed at a rate of 15%. A double tax treaty may provide for lower rates. They will need to be justified. To do this, the recipient of dividends confirms that he is a resident of the country with which the agreement is concluded.

Tax on dividends to individuals

Taxation of dividends with personal income tax is regulated by Art. 214 taking into account the provisions of Art. 226.1 Tax Code of the Russian Federation. And also Art. 210 Tax Code of the Russian Federation. The procedure for calculating and paying personal income tax depends on the legal form of the tax agent:

- JSC - calculates personal income tax in accordance with Art. 226.1 of the Tax Code of the Russian Federation and transfers it to the budget no later than one month from the date of payment of income to the shareholder (without a depository);

- LLC - calculates personal income tax in accordance with Art. 226 of the Tax Code of the Russian Federation and transfers the withheld tax no later than the day following the day of payment of dividends.

Dividend rates for individuals are shown in the table:

| Type of dividends | Bid | Base |

| Received by individual residents of the Russian Federation |

| clause 1 art. 224 Tax Code of the Russian Federation |

| Received by non-resident individuals of the Russian Federation | 15%, unless another rate is established by a double tax treaty | clause 3 art. 224 Tax Code of the Russian Federation |

The tax is calculated using the formula:

N = K × CH × (D1 - D2), where:

- N - amount of tax to be withheld;

- K is the ratio of the amount of dividends subject to distribution in favor of the recipient of dividends to the total amount of distributed dividends;

- Сн - tax rate;

- D1 - the total amount of dividends to be distributed in favor of all recipients;

- D2 - the total amount of dividends received from other organizations (what has changed in 2021?).

When we calculate dividends, we do not provide deductions, that is, they are calculated separately. This applies to all types of deductions: standard, social, property, professional (letter of the Federal Tax Service dated June 23, 2016 No. OA-3-17 / [email protected] ).

Federal Law No. 8-FZ dated February 17, 2021 introduced changes to the calculation of personal income tax on dividends. The amount of income tax withheld from dividends received by a Russian organization is taken into account when calculating personal income tax, which must be withheld from dividends paid in proportion to the share of participation in such an organization to an individual who is a Russian tax resident (clause 3.1 of Article 214 of the Tax Code of the Russian Federation). Read more

If dividends are paid to a non-resident foreign individual, the formula is applied: Н = К × Сн × Д1.

Dividends to non-residents can be paid in foreign currency (Article 6 of Federal Law No. 173-FZ dated December 10, 2003, clause 1 of the Bank of Russia Information Letter No. 31 dated March 31, 2005). There is no need to issue a transaction passport. Expenses in the form of negative exchange rate differences are classified as non-operating expenses (subclause 5, clause 1, article 265 of the Tax Code of the Russian Federation).

Alimony from the income of the LLC founder

As already mentioned, the income of the founder of the organization is dividends, which are paid to him no more than once every three months. For this reason, when withholding funds from such dividends, it is necessary to take into account the frequency of receipt of income.

From the salary of the founder, who himself works in the LLC, maintenance amounts are withheld in accordance with the general procedure. It all depends on the holding order. Thus, the legislation allows the following methods of retention:

The procedure and amount of alimony payments can be established:

- agreement of the parties;

- court order.

The established amount of maintenance is withheld on a monthly basis. So, everything is clear with wages: deduction is carried out monthly in accordance with the established amount.

Dividends are paid every three months. Alimony from dividends is also withheld on a monthly basis, but directly on the day of dividend payment, whatever the frequency.

For example, if the company has established a payment frequency of six months, then maintenance amounts will be withheld for 6 months.

Alimony by agreement

Or, through an agreement, it can be established that a certain percentage of dividends will be withheld as maintenance. Withholding is carried out immediately at the time of payment of dividends.

However, in the situation with dividends, it also happens that they are simply not paid. The organization does not always carry out successful business activities. So, if the LLC does not make a profit, the payer will be forced to pay maintenance as a percentage of the average salary in the country.

Alimony in equity

Alimony, by definition, is established in proportion to the income of the payer. The size of this share depends on the number of children. When an agreement regarding payment has not been drawn up between the parties, they are tied to the payer’s salary in the following shares:

- for an only child - a quarter;

- for two - a third;

- for three or more - half.

However, this is not a strictly designated size. It can be increased or decreased in court. But this requires good reasons. For example, to reduce the amount of payments, such a basis could be the deterioration of the financial condition of the alimony provider.

For an increase, the basis may be the children’s actual need for money. For example, if a child suffers from a chronic disease, is disabled, etc., then the court may increase the amount of payments.

Alimony in a fixed amount

The law establishes the following list of grounds on which maintenance amounts can be fixed and not tied to regular income:

- the person does not have a regular income;

- the person has income in kind, in the currency of another country;

- when a person has no profit at all;

- if the designation as a share of the salary violates the rights of the parties;

- when each party has children.

When determining the fixed size under consideration, one must proceed from:

- the need to preserve for children the amount of maintenance that was provided before the designation in fixed terms;

- from the average salary in Russia, if previously alimony was not paid as a share of the salary.

The court also has the right to take into account other circumstances of the financial and marital status of the parties.

Difficult situations in taxation of dividends

When paying dividends, unusual situations occur. For example, you decided to issue dividends in goods or the recipient refused dividends. With taxes, everything will not be so clear here. Let's look at popular questions.

Dividends from previous years

Many people are interested in whether dividends can be paid using retained and unpaid profits from previous years. You can, and in this case you don’t have to wait until the end of the quarter or year. But in the decision on payment, it is important to indicate for what year and in what amount the profit is distributed.

Personal income tax is withheld at the rate that is in effect on the date of payment of dividends.

Withdrawal from the founders

How to pay dividends if a participant left the founders and the share transferred to the company? The Tax Code of the Russian Federation states that this must be done proportionally. Before the distribution of shares among the remaining participants, dividends can be paid to them disproportionately to their shares only if the participants themselves decide so or such a procedure is provided for by the charter.

Amounts exceeding the amount of dividends proportional to the share are not recognized as dividends for tax purposes (letter of the Ministry of Finance dated July 30, 2012 No. 03-03-10/84). This indicates that the tax rate will change. If you pay dividends, then the rate is 13%, and if the payment is not recognized as dividends, the rate is 20%. This is especially important with non-resident individuals: the rate can increase from 15% to 30%.

The Ministry of Finance says that if the payments are not recognized as dividends, then they also do not need to be shown as dividends in 6-NDFL. Other rates may apply and deductions may apply. Therefore, the tax office is interested in how you pay dividends: proportionally or disproportionately.

Waiver of dividends

What should I do if a participant asks to replace dividends with a fixed monthly compensation? How to distribute dividends and what to do with personal income tax?

The Ministry of Finance believes that since the participant does not want to receive dividends, then he gave them to you. At the same time, he must pay personal income tax, even if he refused to pay (letter of the Ministry of Finance dated October 23, 2019 No. 03-04-06/81252). The action algorithm is as follows:

- On the day the participant refuses dividends, calculate personal income tax from the “refused” amount;

- Withhold personal income tax from the compensation amount monthly (you can reduce it by deductions);

- Do not charge insurance premiums.

Determine when dividends can be distributed without harming the company - make management decisions based on the numbers

Try for free

Refusal to pay the actual value of the share

The former participant may refuse to pay the actual value of the share upon leaving the company. The courts consider this as debt forgiveness (Resolution of the Federal Antimonopoly Service of the North-Western District dated May 16, 2012 No. F07-3024/12).

The Ministry of Finance repeatedly says in its letters that the cost of the share that was abandoned is included in the organization’s non-operating income (letter of the Ministry of Finance of the Russian Federation dated October 2, 2018 No. 03-03-06/1/70715, etc.). It would seem, why is this income if we have already paid tax once when we calculated net profit? But regulatory authorities think differently.

Incorrect details for dividends

The founder did not provide new details. Dividends were transferred to him, but due to incorrect details, the entire amount was returned to the account. At the same time, personal income tax was withheld and paid to the budget.

Paid tax can be refunded. To do this, reflect the return of dividends in your accounting records, reverse the withheld personal income tax and submit an updated calculation of 6-personal income tax. At the same time, send a tax application, an extract from the personal income tax register and a payment order for tax payment. Personal income tax can be offset against future payments or returned to the account (letter of the Federal Tax Service dated 02/06/2017 No. GD-4-8 / [email protected] ).

Crediting a loan against dividends

The organization issued a loan to the founding legal entity. It will be repaid by offset of dividends due. How to arrange this?

The amount offset against the debt must be indicated in the income tax return as dividends actually received (clauses 5.3, 6.3 of the Procedure, approved by Order of the Federal Tax Service dated September 23, 2019 No. ММВ-7-3 / [email protected] ):

- in non-operating income on line 100 of Appendix No. 1 to sheet 02. The data in this line is transferred to line 020 of sheet 02;

- in income excluded from profit on line 070 of sheet 02.

And all this must be shown on the day of signing the agreement on offsetting mutual claims.

Dividends in kind

Dividends can be paid not only in money, but also in property. Elena Danyakina, a tax consultant, spoke about the peculiarities of taxation and the cases in which this is permissible in the Kontur.School webinar “Dividends in 2021. How to calculate, distribute, and withhold taxes.”

In short, you can pay dividends with property. But to avoid disputes with the tax authorities, it is advisable to enshrine this in the charter or approve it in the decision of the general meeting on the payment of dividends. In order to then calculate income tax and adjust the financial result, the founders should determine the monetary value of the transferred property. Personal income tax on dividends in kind will be paid by the recipient.

Receiving dividends from a foreign organization

Dividends from any organization, including a foreign one, are taken into account as part of non-operating income (clause 1 of Art. , clause 1 of Article 250 of the Tax Code of the Russian Federation). However, if they are paid by a foreign organization, then the Russian company itself calculates and pays income tax (clause 2 of Article 275 of the Tax Code of the Russian Federation).

Income tax is reduced by the amount of tax that was withheld from dividends at the location of the foreign company, but only if this is provided for in an international treaty between the Russian Federation and that country.

How much credit can I receive? When paying income tax in the Russian Federation, a Russian organization can receive a credit in an amount not exceeding the amount paid in the Russian Federation. For example, if you paid 15,000 rubles from dividends abroad, and at the Russian tax rate the tax is 13,000 rubles, then you can only take 13,000 rubles as a credit, and the remaining 2,000 rubles cannot be offset and written off as income tax expenses ( Letter of the Ministry of Finance dated May 31, 2017 No. 03-12-11/3/33520).

Conditions for registration:

- there is an international agreement or treaty on the avoidance of double taxation;

- payment of tax abroad is confirmed by documents;

- simultaneously with the income tax return, a declaration on income received outside the Russian Federation is submitted;

- At the end of the period, your organization has no loss.

If you receive dividends in foreign currency, you must convert them into rubles at the rate of the Central Bank of the Russian Federation on the date of receipt (clause 5 of Article 210 of the Tax Code of the Russian Federation).

General director salary 10 thousand how to collect alimony

- a copy of the salary certificate of the person liable for alimony (it can be obtained from the bailiff conducting your enforcement proceedings);

- a copy of the response from the government agency. statistics with information on average wages in the labor sector of interest to us in the region;

- a thesis statement of the situation in connection with which this appeal was needed:

- when alimony was collected;

- what amounts are paid monthly?

The rules for collecting alimony in percentage form for each child are prescribed in the text of Article 81 of the Family Code of the Russian Federation. The following documents will help you prove the lack of alimony:

- Certificate from the claimant’s place of work or employment center;

- Receipts for payment to an educational institution (kindergarten, school, lyceum, etc.);

- Receipts for payment of additional education (tutors, clubs, sections);

- Receipts and prescriptions for the purchase of vital medications;

- Receipts for clothing, toys, stationery and educational supplies for each month to identify average expenses.

Please note that you need to divide the amount received in half (for yourself and your ex-husband), and if alimony from a gray salary does not cover the specified part, then feel free to contact the bailiff service or the court at your place of residence

Dividends in the income tax return

If you pay dividends to Russian organizations, you need to submit an income tax return to the tax office. This also applies to tax agents using the simplified tax system. In addition to standard sheets, it includes:

- subsection 1.3 section 1, which shows the amount of tax payable to the budget, according to the tax agent;

- sheet 03 “Calculation of income tax withheld by the tax agent”, which is filled out for each decision on the distribution of dividends (in section “A” the tax on income in the form of dividends is calculated, in section “B” the amount of dividends paid to each shareholder is indicated ( participant).

Fill out, check and submit your income tax return online

Try for free

Let's look at filling out section “A” of sheet 03 using an example.

Example . JSC Omega is the sole founder of Sigma LLC. In December of this year, Omega receives dividends of 70,000 rubles.

In September of this year, Omega JSC accrued and paid interim dividends to its shareholders - 253,000 rubles. At the same time, 55,000 rubles were paid through the depositary, and 198,000 rubles were paid independently:

- 110,000 rubles - to a legal entity;

- 88,000 rubles for resident individuals.

In sheet 03 of the income tax return this is reflected as follows:

How to show dividends on sheet 03 of the income tax return

The amount of dividends for calculating tax (line 091) is determined as follows:

The total amount of dividends is 253,000 rubles, of which:

- legal entities - 110,000 rubles (43.478%)

- depositary - 55,000 rubles (21.739%)

- individuals - 88,000 rubles (34.783%)

The distributed amount of dividends is 183,000 rubles (253,000 - 70,000).

The declaration includes income tax on dividends to legal entities:

- 183,000 rubles × 43.478% = 79,565 rubles

- 79,565 × 13% = 10,343 rubles

If dividends are paid to a foreign company, then only the amount of accrued dividends is reflected in the income tax return. The Federal Tax Service also submits “Calculation of the amounts of income paid to foreign organizations and taxes withheld.” It is submitted within the same time frame as income tax returns - no later than 28 calendar days from the end of the reporting period (clause 4 of Article 310 of the Tax Code of the Russian Federation, letter of the Ministry of Finance dated October 10, 2016 No. 03-08-05/58776 ).

Collection of alimony from the founder of an LLC

The collection of alimony from the founder of the company can be carried out either voluntarily or compulsorily. If the obligation to pay alimony is fulfilled voluntarily, the parties most often make mutual settlements based on a notarial agreement.

In case of forced collection, the rules for fulfilling obligations are determined by a court order. At the same time, when the payer does not comply with this resolution, the collection is carried out according to the executive document.

This executive document must be sent to the person directly making the payments. As a rule, this is the accounting department of the organization.

USEFUL INFORMATION: What documents confirm the fact of living together between spouses and what form they should be

However, the recipient has the right to send a similar document to the bailiffs. This usually happens when a company does not pay dividends. In such a situation, they collect at the expense of other money of the payer, as well as property.

Thus, alimony is withheld from the income received by persons as a founder of the company. This takes into account the specifics of the dividend payment procedure in the relevant organization.

Dividends in 6-NDFL

When paying dividends to individuals, tax agents submit 6-NDFL calculations. An updated form has been in effect since 2021. For a detailed analysis of the changes, see the article “New form of calculation of 6-NDFL from 2021”.

In 6-NDFL, dividends are included in sections 1 and 2 of the calculation for the period in which the payment was made:

- in fields 110, 111 of section 2 - the full amount of dividends distributed in favor of individuals participating in the organization;

- in fields 140 and 141 of section 2 - the amount of personal income tax calculated on dividends (before it is reduced by the amount of income tax);

- in field 160 of section 2 - the amount of personal income tax calculated from dividends and reduced by the amount of income tax subject to offset when determining the amount of personal income tax payable on the basis of clause 3.1 of Art. 214 Tax Code of the Russian Federation;

- in fields 020, 022 of section 1, you must reflect the amount of personal income tax calculated from dividends and reduced by the amount of income tax subject to offset.

The amount of tax withheld for the last three months of the reporting period, specified in field 020 of section 1, must be equal to the sum of the values of all fields 022. That is, the amount of tax withheld in previous periods, despite the fact that the payment deadline came in the current period, in the new form in the first quarter of 2021 is not indicated. Therefore, the organization should reflect the dividends paid in December in section 2 of the 6-NDFL calculation for 2021.

The procedure for filling out 6-NDFL when paying more than 5 million rubles was discussed by the Federal Tax Service in a letter dated March 30, 2021 No. BS-4-11/ [email protected]

Dividends received by an individual, minus the amount of income tax to be credited, should be included in the “Amount of Income” field of the application “Information on income and corresponding deductions by month of the tax period.” Income code - 1010 (letter of the Federal Tax Service dated April 13, 2021 No. BS-4-11/4999).

Fill out the current form 6-NDFL with tips and checking against control ratios

Try for free

Income of the LLC founder

A limited liability company is a form of establishment of an organization that engages in commercial activities.

The founders of such an organization can also be individuals. Civil legislation establishes that the founders are the owners of the company, including its profits. So the profit of the company is the income of the founder, from whom alimony can be withheld. So you cannot receive alimony from an LLC. For example, during the forced collection of funds, it is impossible to seize the accounts of an organization whose founder is the payer. But if the payer is an individual entrepreneur, then collection can be carried out from his business accounts.

Thus, dividends received based on the results of the company’s activities are the only income of the founder. They cannot be paid more frequently than once every three months.

But, as a rule, the founders often occupy key positions in the LLC. In this case, they also receive wages. Such income is also taken into account when calculating the amount of maintenance. For example, alimony is withheld from the director of an LLC from both dividends and salary.

Thus, the income of the founders of the company can be varied. So you need to understand the procedure for calculating the size of the content.

What has changed in 2021

In 2021, new forms of income tax declaration and calculation of 6-NDFL appeared, a progressive income tax rate was introduced, and the rules for calculating dividends changed.

Change No. 1. New rules for calculating D2

From 2021, indicator D2 (dividends received by the tax agent itself) excludes any dividends taxed according to the Tax Code of the Russian Federation at a rate of 0%, as well as dividends from foreign entities to which the Russian taxpayer has the actual right and which were exempt from taxation in Russia ( Federal Law of November 23, 2020 No. 374-FZ, paragraph 5 of Article 275 of the Tax Code of the Russian Federation).

Change No. 2. Increased personal income tax rates

The calculation of personal income tax on dividends will be made on an accrual basis from the beginning of the tax period (Federal Law No. 372-FZ dated November 23, 2020). Personal income tax rate on dividends:

- 13% - if the tax base for dividends does not exceed 5 million rubles inclusive;

- 15% - in relation to the tax base for dividends exceeding 5 million rubles.

From 2023, the totality of tax bases will be considered. If now we look separately at dividends, separately at wages - whether they exceeded or did not exceed, then we will look at the total amount.

Amount of alimony

But judicial practice shows that in some situations the method of calculating alimony as a percentage of income violates the legal rights and interests of the child. For example, if an organization, according to documents, incurs losses without making a profit, then alimony from dividends is not collected. As a result, the child may receive 1-2 thousand rubles from the salary of the child support provider, which does not satisfy the needs of the minor, but at the same time complies with the law.

There are other options for collecting alimony.

- In a fixed amount, which depends on the cost of living parameter established in the region of residence of the parents. When this indicator increases, the amount of alimony also increases, and when it decreases, the amount of alimony payments does not change. Usually the court sets alimony at a minimum of 4 thousand rubles.

- In a combined way - as a percentage of income and in a fixed amount. This is the most optimal way to collect alimony from the director of an LLC. Alimony in % will be collected from a fixed salary, and a fixed amount - from non-permanent dividends.

If the financial and/or marital status of the recipient of the funds or the alimony provider has changed, then both parties have the right to go to court with a demand to increase/decrease the amount of alimony.