Any officially employed citizen has the right to go on vacation paid for by the employer once a year, but this right must be earned. There are various situations in life in which it may be necessary to urgently apply for leave or there is a strong desire to interrupt your work experience for a vacation ahead of schedule. Some categories of employees want to add early leave to their due leave, for example, maternity leave, or to quit immediately after the rest.

- Can an employer meet such wishes of employees, does this not contradict the requirements of the Labor Code, and what does he risk in doing so?

- Does he have the right to refuse outright?

- How to arrange “vacation in advance”?

Let's understand the nuances.

The concept of “vacation in advance” and its legislative framework

There is no official term “vacation in advance” in Russian legislation. Annual paid leave, guaranteed to each employee by the Labor Code (Article 122), is earned for 1 working year. It is counted not from the beginning of January, but from the date of registration of the employment contract, that is, it is individual for each employed person.

An employee can go on this leave after completing six months of work experience (the provisions of Article 122 of the Labor Code of the Russian Federation) or earlier, in agreement with the employer. It is not difficult to calculate that during this time, at best, only half of the officially established vacation duration will be worked. It turns out that the second half, if the vacation is not divided into parts, the employee receives in advance.

If the length of service is less than 6 months, then the advance payment of vacation days provided is even longer.

In the second and subsequent years of work, vacation is given according to the schedule at any time; length of service no longer matters, so vacation is often assigned in advance.

FOR YOUR INFORMATION! International Labor Organization Convention No. 132 on Holidays with Paid, which the Russian Federation ratified in 2010, states that an employee can receive leave from any day of his employment for a duration proportional to the time worked. However, many employers give preference to the norms of the Labor Code of the Russian Federation, which are legally “above” the conventional ones. The Labor Code does not deprive the employer of the right to allow early leave, and, regardless of the time worked, it allows you to receive it in full.

Thus, it is possible to define leave provided in advance as annual paid time for legal absence from the workplace, received before the moment of its actual working out.

Calculation of vacation pay

Vacation benefits are calculated using a standard formula. The most interesting point in this situation is the issue of calculating unworked days.

Detailed example:

Goncharova I.V. got a job at Romashka LLC as a specialist in the sales department, and after 6 months and 7 days she decided to quit. At the same time, Goncharova used all the rest days completely - 28 days. In order to start the calculation, you should round and set aside seven days. It turns out that after working for six months, Goncharova had the right to annual leave.

How many days did she work? For this, the following formula is used: 2.33xZ, where Z is the number of complete months worked. Thus, it turns out to be 13.98. It is customary to round in favor of the employee.

Hence the conclusion: Goncharova had the right to only 14 days of rest. Consequently, from her severance pay upon dismissal, the accounting staff will withhold the amount for 14 days that were used in advance. When withholding, you must proceed from the rule: the amount should not exceed 20% of each salary.

Differences between advance leave and timely leave

The conditions under which such a vacation becomes a reality differ from the usual guarantee of annual vacation in several important nuances:

- the manager has the right to refuse permission for such leave, since providing rest in advance is not his responsibility;

- vacation granted in advance cannot be replaced with monetary compensation, because these funds have not yet been earned;

- like regular leave, such leave can be divided into parts, one of which cannot be less than 2 weeks.

What types of holidays cannot be provided in advance?

Not all types of vacations can be taken off earlier than expected. The concept of “vacation in advance” most often refers specifically to annual vacation paid by the employer. But there are some types of leave that must have a documentary basis, so they cannot be granted in advance if the employee does not have an official document confirming this basis. Such holidays include:

- additional;

- administrative;

- training;

- maternity leave (both for childbirth and for caring for the baby).

Vacation before or after another vacation

Motherhood is such a special event in a woman’s life that the state tries in every possible way to protect this category of workers. Women planning maternity leave have the right to go on another vacation, even without having worked for the organization for the required 6 months. Mothers can receive the same leave immediately after leaving maternity leave.

In addition to pregnant women and young mothers, the right to go on leave regardless of length of service is granted to:

- their spouses;

- relatives if they took maternity leave instead of their mother;

- employees who have two young children under the age of 14;

- fathers and mothers of disabled children under 18 years of age.

The law provides the same right, but for reasons not related to parenthood:

- part-time employees who are granted leave from their main job (it must coincide with the rest from their combined position);

- wives or husbands of military personnel who have received their leave (for military spouses, the vacation time must also coincide);

- other categories of employees for whom this right is provided for by the organization’s labor or collective agreement.

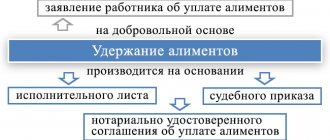

How to register and take into account

Registration is carried out in full accordance with the general rules: first, the worker writes an application (if there is a schedule, this is not necessary), receives an employer visa, an order is drawn up, and appropriate deductions are made. The benefit is also calculated according to general rules, based on the established amount of average monthly earnings. And it is paid in full for all days provided, regardless of how many days of rest the employee is entitled to, in proportion to the actual time worked in the organization. Appropriate notes are made in the work schedule and time sheet.

Vacation before dismissal

Before finally leaving the workplace, the employee has the right to “take off” his allotted vacation days. But what if he plans to quit without earning enough experience for a vacation, but nevertheless wants to go on it?

The key point is the employer's consent. If the management does not mind providing the employee with such an opportunity, nothing prevents him from continuing to be listed as an employee of the company during his vacation, having completed the resignation documents on his last working day. However, it should be remembered that before going on vacation, the issue of monetary compensation for vacation not earned by the resigning person must be resolved: it will have to be paid into the cash register voluntarily, or it will be deducted from the salary during the calculation. The employer will not be able to demand this if the employee quits for one of the following reasons:

- consent of the parties (all issues, including payment, are resolved mutually before the order is issued);

- expiration of the employment contract;

- transfer to another place, to another employer;

- changes in working conditions and refusal to cooperate associated with changes;

- sick leave for more than 4 months (except for maternity leave);

- the employee is sent by the company for training;

- the employee was “laid off”;

- the court reinstated the employee who had previously occupied the position of the dismissed person;

- An employee who has rested in advance retires.

NOTE! If an employee leaves voluntarily or quits due to culpable behavior, compensation for unworked but “committed” vacation can be deducted from his salary without asking consent.

Insurance premiums

The employer calculates insurance premiums in the general manner from the amount of vacation pay (clause 1 of Article 420 of the Tax Code of the Russian Federation).

The base for insurance premiums is calculated on an accrual basis from the beginning of the year until the end of the corresponding month (clause 1 of Article 431 of the Tax Code of the Russian Federation). Since, in connection with the withholding (return) of the amounts of unpaid advance payment, the amount of previously calculated insurance premiums is reduced, the employer is not required to submit an updated Calculation of insurance premiums (clauses 1, 7, Article 81 of the Tax Code of the Russian Federation). However, it is necessary to adjust the liability for insurance premiums. Since contributions are considered a cumulative total from the beginning of the year, it is believed that adjustments to contributions in connection with the withholding (return) of vacation pay for unworked days can be made in the current period. However, this approach is not entirely correct and does not take into account the situation when an employee voluntarily returns amounts in an amount greater than the final payments upon dismissal. After all, negative values in the calculation of insurance premiums are not allowed (Letter of the Federal Tax Service of Russia dated August 24, 2017 N BS-4-11 / [email protected] ).

In addition, information from Section 3 of the Calculation of Insurance Premiums must be correctly reflected in the individual personal accounts of the insured persons. In this regard, there is a need to adjust the amount of vacation pay in the period in which they were initially accrued, as indicated, for example, in paragraph 2 of Letter of the Federal Tax Service of Russia dated October 11, 2017 N GD-4-11/20479. This option is recommended to be used in any case (even if the dismissal payments are enough to withhold) so that the information from the Calculation of Insurance Premiums is comparable with forms 2-NDFL and 6-NDFL.

If the organization refuses to make deductions or is unable to make them due to restrictions, no adjustments need to be made to the calculation of insurance premiums, since the amounts of previously calculated contributions do not change (Letter of the Ministry of Finance of Russia dated July 26, 2018 N 03-15-06/52554) .

Pitfalls of “advance leave” for the employer

It is not surprising that some employers choose not to deviate from their right to provide holiday only on time. There are certain risks in the fact that an employee goes on vacation without earning this opportunity.

The main problem for employers is the possibility of losses due to amounts overpaid for unworked vacation. The manager may face difficulties withholding funds in the event of dismissal of an “over-rested” employee. An employee does not always agree to compensation for vacation pay of his own free will, while it is very difficult to claim this money in court. The law mainly protects the interests of workers, and the regulations provide for a large number of circumstances to which the claim for compensation does not apply, for example:

- the amounts due before dismissal are not enough to cover the debt;

- if the deduction is not made directly upon dismissal, you will have to act through the court or accept the loss of money, the employer has no other legal ways to force the employee;

- the reason for dismissal excludes the possibility of claiming the debt.

Personal income tax

The amounts of paid vacation pay are employee income subject to personal income tax (clause 6, clause 1, article 208, clause 1, article 210 of the Tax Code of the Russian Federation). Personal income tax is calculated on the date of actual receipt of income, determined in accordance with Art. 223 of the Tax Code of the Russian Federation (clause 3 of Article 226 of the Tax Code of the Russian Federation). In relation to vacation pay, such a date is the day of payment of income (transfer to the employee’s card or issuance in cash through the cash register) (clause 1, clause 1, article 223 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated March 28, 2018 N 03-04-06/19804, Letter Federal Tax Service of Russia dated 06/13/2012 N ED-4-3/ [email protected] together with Letter of the Ministry of Finance of Russia dated 06/06/2012 N 03-04-08/8-139).

Personal income tax is withheld directly from the taxpayer’s income when it is actually paid to the employee (clause 4 of article 226 of the Tax Code of the Russian Federation). Personal income tax on vacation pay is transferred no later than the last day of the month in which such payments were made (clause 6 of Article 226 of the Tax Code of the Russian Federation). If any deductions are made from the taxpayer’s income by order, by decision of a court or other authorities, such deductions do not reduce the tax base (paragraph 2, clause 1, article 210 of the Tax Code of the Russian Federation).

According to the explanations of the Ministry of Finance, if an employee returns to the employer the amounts of vacation pay actually paid to him earlier, such amounts will not be recognized as his income.

Personal income tax amounts withheld and transferred to the budget from the specified vacation leave are overpaid by the tax agent. Accordingly, the amount of the employee’s personal income tax obligations for the tax period must be adjusted. At the same time, the tax agent - employer has an overpayment of personal income tax, which can be returned to him within the framework of Article 78 of the Tax Code of the Russian Federation (Letter dated October 30, 2015 N 03-04-07/62635 (sent by Letter of the Federal Tax Service of Russia dated November 11, 2015 N BS- 4-11/ [email protected] )).

The Federal Tax Service, in turn, explains that in the case when an organization (tax agent) recalculates the amount of vacation pay and, accordingly, the amount of personal income tax, then in section 1 of the calculation in Form 6-NDFL the total amounts are reflected taking into account the recalculation made (Letter of the Federal Tax Service of Russia dated 05/24/2016 N BS-4-11/9248). The Letter of the Federal Tax Service of Russia for Moscow dated March 12, 2018 N 20-15/049940 clarifies that the total amounts, taking into account the recalculation made, are reflected in Section 1 of the updated calculation in Form 6-NDFL for the period in which vacation pay was accrued. Thus, if by the time of recalculation of vacation pay you have already submitted Form 6-NDFL, it must be adjusted by entering the amount of vacation pay, taking into account the withholding (refund) of tax.

Certificates in form 2-NDFL also need to be adjusted if you have already submitted them by the time of recalculation. If not, the final data must be generated taking into account recalculation.

The specified approach is presented in paragraph 1 of the Letter of the Federal Tax Service of Russia dated October 11, 2017 N GD-4-11/20479.

If the employer does not withhold vacation pay for unworked days (of his own free will or due to legal restrictions), no adjustments need to be made to personal income tax reporting. After all, personal income tax has already been withheld from the employee’s income, while vacation pay remains vacation pay (payments are not reclassified). The employee does not receive additional income. On this issue, see Letters of the Ministry of Finance of Russia dated December 26, 2017 N 03-04-06/86736 and the Federal Tax Service of Russia for Moscow dated June 28, 2018 N 20-15/138129.

“Paper” registration of early leave

It is no different from the traditional one, the sequence of actions remains usual:

- An employee writing a statement.

- Positive endorsement of the application by management.

- Issuing an order to grant leave.

- Accrual of “vacation” funds (the only difference is that they have not yet been earned).

ATTENTION! If the employee has been working for more than a year, then the first point will be preceded by scheduling vacations.