Restriction of freedom of contract by the Family Code

The agreement may include any terms. For example, a marriage contract when purchasing an apartment may provide for the sole ownership of the spouse in whose name it is registered. The transfer of rights from one of them to another upon the occurrence of a certain event may be stipulated: the birth of a child, the acquisition of another home, divorce.

As a general rule, “an agreement is more valuable than money,” but this does not always apply to a marriage contract. According to Article 44 of the RF IC, it can be declared invalid (in a separate part or in its entirety) if the transaction meets the general criteria of invalidity established by the Civil Code (coercion, incapacity of persons, other violations).

Second: at the request of one of the spouses, the court may recognize the marriage contract for an apartment or other property as invalid if its terms “put the other spouse in an extremely unfavorable position” (Clause 2, Article 44 of the Family Code). Thus, freedom of choice can be “crossed out” at the discretion of the court.

What to consider in the text when drawing up a mortgage agreement?

It is permissible to register only property agreements of the parties. Please note that a contract that is written in the interests of only one spouse and does not take into account the interests of the second can be challenged and declared invalid.

The agreement is prescribed both for property already owned by the spouses and for that which will be acquired in the future. It is important to specify the terms of agreements and terms of execution.

The agreement required by the bank to obtain a loan must establish:

- which spouse is the borrower;

- who bears the financial costs when paying the down payment and applying for a loan;

- how the mortgage housing will be divided in the event of a divorce;

- who will make further payment of contributions;

- who will be the legal owner of the living space.

Prenuptial agreement for an apartment purchased before marriage

Almost everyone knows that property acquired before the wedding, gifted to one of the spouses, or received by inheritance is not subject to the common property regime. Therefore, they consider it not necessary to mention in the marriage contract an apartment purchased before marriage. Problems arise when it is sold and other housing is purchased with the money received, sometimes with the addition of borrowed funds.

During a divorce, the spouse claims half of the property. In this case, you can defend your rights only if you prove the personal ownership of the funds. These could be documents of donation, certificates for an old apartment and a contract for its sale with the subsequent execution of a purchase and sale transaction for shared housing.

Example. Determination of the Supreme Court No. 4-КГ16-37 (from Review of Practice No. 2, approved 04/26/2017).

The spouses did not draw up a prenuptial agreement for the apartment purchased during marriage. Meanwhile, it was purchased with the wife’s own money, proceeds from the sale of another one, previously given to her by her mother (the documents were drawn up correctly). The amount of investment corresponded to 14/15 of the cost of the premises. After the divorce, the husband filed a claim for the allocation of ½ of the apartment. Let us note that the courts of the first and appellate instances satisfied the requirement, based on the fact that the spouse voluntarily invested money in common housing and did not object to its registration as common shared property. The Supreme Court put an end to the dispute by ruling that contributing funds to purchase a shared apartment does not change the essence of their origin. They were received as a result of a gratuitous transaction and belong to the personal property of the spouse.

Thus, a prenuptial agreement for an apartment purchased before marriage relieves the owner of many problems in the event of a divorce. In the example above, the litigation lasted more than 3 years. Previously, practice was in favor of dividing the disputed premises in equal shares. Especially if documents confirming the origin of the money have been lost. After all, quite often parents give them to their children without filling out anything, not even a receipt in case of a loan.

Advantages of a prenuptial agreement

However, we should not forget about the advantages of prenuptial agreements. With their help, you can bypass marriages for the sake of property. It is not so rare that there are cases when one party is successfully running a business, while the other is still studying. If you first stipulate that your spouse does not claim the second half of your space, there may not be a wedding. Prenuptial agreements also reduce the number of marriages with large age gaps.

A marriage contract does not provoke divorce, but on the contrary, in many cases it prevents it. Since, if in a non-contractual family a husband or wife can separate without holding back their emotions, then with a marriage contract you will think: Because in this case, each of the spouses loses the corresponding part of the joint property. The number of divorces due to suspicious reasons will also decrease. If the marriage contract is drawn up correctly, taking into account the interests of both parties, the spouses will not even think about divorce. And upon divorce, each spouse will spend considerable money to achieve freedom.

Marriage agreement for an apartment purchased during marriage

As already noted, spouses can draw up an agreement at any time. And a prenuptial agreement when buying an apartment will not be superfluous if they want to avoid a subsequent “division” through the court. Thus, it often provides for the following conditions:

- registration of the purchased apartment as the sole property of one of the spouses, when personal funds are spent on this;

- transfer of rights to the spouse if, by the time of divorce, the family has common children;

- transfer of the right of existing housing to one of the family members if another apartment (house) is purchased.

The choice of options is unlimited, but, as practice shows, spouses often lack forethought and life experience. Thus, in our practice, there was a case when a husband persuaded his wife, under the pretext of buying a new home, to enter into an agreement, under the terms of which all the real estate was re-registered to him. After which he filed for divorce, and all her attempts to challenge the deal were unsuccessful.

If the contract is developed properly, neither spouse will be interested in creating a divorce situation. Lawyers and advocates of our company will help you competently draw up a prenuptial agreement for an apartment purchased during marriage, taking into account all possible consequences, including the possibility of challenging it in court. And this is especially necessary when housing is purchased with a mortgage and third parties are involved in the dispute (bank, AHML and others).

What documents are needed to draw up a contract?

In accordance with Art. 38 and 40 of the RF IC, a marriage contract is always drawn up in writing and must be certified by a notary office.

At the same time, the notary not only certifies this document, but also studies it for compliance with the laws, so it is necessary to provide him with documents to cover the full picture of the property relations of the spouses. The agreement is drawn up in three copies, one for the spouses, one for the notary.

Depending on whether the apartment has been purchased or the spouses are just planning to purchase it, it will depend on what package of documents needs to be prepared.

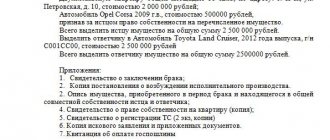

If the apartment is already owned, you will need:

- Spouses' passports.

- Marriage certificate.

- Confirmation of ownership rights - a purchase and sale agreement and a certificate of ownership or an extract from Rosreestr;

If you have yet to purchase an apartment, then instead of documents establishing the rights to the existing housing, you need to attach the following:

- Preliminary agreement for the purchase of real estate;

- If you are taking out a mortgage, you will need a loan agreement;

- When purchasing an apartment in a new building - an agreement for participation in shared construction.

To certify a marriage contract, you need to pay a fee (the rate for a private notary is about 500 rubles) and pay a service fee, which varies from 5 to 10 thousand rubles. It depends on whether the services include only contract certification or also drawing up a draft contract, as well as technical work.

Marriage agreement when buying an apartment with a mortgage

This is the best way to settle debts in case of divorce. Because a loan is sometimes issued for 10–30 years, and no one can be sure in advance that the marriage will not break up during this time. Let's consider two general cases.

- The apartment was purchased with a mortgage before marriage. In this case, it is not considered common property. However, the debt at this point can reach from 10 to 90% of its value. In the event of a divorce, the second spouse may claim a share of housing corresponding to half of the payments made during the period of marriage. This, of course, may not suit the person who actually paid the debt and interest.

- Housing was purchased during marriage, but a marriage contract was not drawn up when purchasing an apartment with a mortgage. Until the end of the loan agreement, the spouses remain equal owners, and it is almost impossible to obtain the bank’s consent to divide the property. The Family Code establishes that debts are divided in proportion to the share of property received after a divorce. As a result, one of the spouses often has to pay the rent. Debts can only be collected from the second person in court, and then only on the condition that the payer will note in the bank the fact that he is solely responsible for paying off the debts.

Given the severity and length of litigation when dividing property, lawyers advise families to settle issues related to real estate in advance and always draw up a prenuptial agreement before receiving a loan.

The document usually stipulates the following conditions:

- the contribution of each spouse in the down payment;

- share of payment in monthly contributions (during marriage and after divorce);

- change in conditions after the birth of the child (children);

- compensation for payments for an apartment in case of divorce;

- determination of the final owner of the property.

At the same time, a marriage contract when purchasing an apartment with a mortgage may contain conditions only in relation to this specific property, without affecting anything else.

Note that banks welcome this practice, and some of them insist on concluding a prenuptial agreement for a mortgage. Even when one of the spouses is the acquirer, they include the other as a co-borrower. This reduces their risk if one of them becomes insolvent.

A prenuptial agreement for a mortgage apartment must be drawn up very carefully, with the participation of an experienced lawyer. Courts often take different positions in disputes involving such real estate, as the examples below show. In this case, two different decisions were made on the same issue: can a marriage contract for a mortgage be declared invalid if its conclusion was a necessary condition for obtaining a loan?

Example 1. Decision of the city court of the Novosibirsk region in case No. 2-17/13 (dated 01/16/2013).

The prenuptial agreement was drawn up before receiving the loan according to the model proposed by the bank. It included a link to a specific loan agreement and the condition that the apartment would belong to the sole owner - the husband. And also that registering it as common property is impossible under any circumstances. In court, the parties explained that the conclusion of the marriage contract for a mortgaged apartment was not caused by their desire and financial problems. It’s just that otherwise they wouldn’t be able to buy a home. The court assessed the bank’s actions as aimed at solving its commercial interests and coercion into an agreement, which is not allowed under Art. 421 Civil Code of the Russian Federation. The document was declared invalid.

Example 2. Decision of the district court of Samara in case No. 2-4809/2013~M-4395/2013 (10/11/2013).

The claim was filed by the husband after the divorce, since according to the terms of the marriage contract for the mortgaged apartment, it was registered as the sole property of the wife. He asked to recognize the transaction as enslaving on the basis of Art. 179 of the Civil Code of the Russian Federation. The plaintiff argued that this condition was imposed by the bank because he had a bad credit history. However, there was no evidence of this fact. This condition of the bank did not appear in the document, the plaintiff did not apply to other credit institutions, and the urgent need to purchase an apartment using borrowed funds was not proven. The court pointed out that even if all the circumstances it indicated had taken place, when signing the marriage contract for the mortgage, he could not help but understand that he did not have any rights to this apartment. Consequently, his actions cannot be considered forced. Refusal would not entail any property losses for him. The claim was denied.

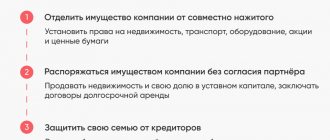

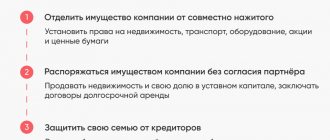

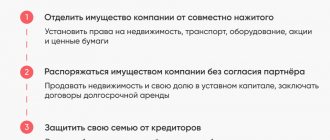

How to Protect Personal Assets with a Prenuptial Agreement

A series of articles about methods and tools for protecting personal assets

In the last article, we figured out how to create an indivisible fund in which you can hide property from creditors, bailiffs, tax authorities and other hunters. This time we’ll look at how a prenuptial agreement (BA) can help protect personal property.

How it works? In the minds of many of our friends, it goes something like this: you are starting to be attracted to a subsidy; you take your spouse and run to the notary; he certifies the marriage contract, according to which the wife gets everything, and you become a newly made homeless person, to the chagrin of your creditors. “It’s logical: she still has children!” - you convince yourself in the evening, drinking whiskey from a crystal glass.

Is it that simple? And are creditors really that stupid and powerless? I will tell you about this below, but for now a disclaimer: we will analyze the database specifically in the context of protecting assets from creditors. If property needs to be protected from a spouse, the effect will be the opposite. By the way, we have recently already talked about what can happen to property when one of the spouses goes bankrupt - this is for a general understanding of the prospects.

What is this anyway?

By default, all property acquired during marriage is the joint property of the spouses. This rule applies to cars, apartments, dachas, businesses, shares, patents, other intellectual property and other tangible and intangible assets. They belong to the spouses in equal shares: each has half and it does not matter to whom it is registered.

An exception to the rule is inherited or gifted property. But if something was inherited by one of the spouses, and the other spouse spent money on maintaining this asset, for example, made major repairs to an apartment, he will be entitled to compensation for these expenses.

Actually, a marriage contract is one of many instruments that changes the property regime of spouses. With the help of a database, the proportion of shares can become not 50 to 50, as provided by law, but, for example, 10 to 90 or something else. For these purposes, you can also use an agreement on the division of property, a settlement agreement, or even divide everything through the court. Each tool has its own pros and cons, its own specifics and scope, but we will talk about this in the following articles.

What are the possibilities inside?

For the database we need Mikhail, his wife Marina and their assets: 1 house, 2 apartments, 3 cars and a wonderful business.

A marriage contract can regulate any property relations between spouses: not only how houses, cars and apartments will be divided, but also income, expenses and maintenance of spouses in the event of a divorce. For example, you can prescribe the payment of alimony or compensation for a share in a jointly purchased apartment. Sometimes this is extremely important.

A prenuptial agreement can be drawn up both before and during marriage. In the first case, the contract will come into force only after the marriage is registered.

An important nuance - if the spouses incurred any debt before signing the marriage contract, creditors must be notified about it. For example, if Marina took out a loan before marriage and still hasn’t paid it off, her bank should be aware. Otherwise, the bank will be able to challenge the database in part or in full. This is especially true if, within the framework of the database, the rights of the creditor are somehow infringed: for example, Marina promises to give 90% of her salary to her spouse for his personal use and then stops paying the loan.

With the help of the database, you can change the regime of joint ownership provided for by law - this is when everything is divided in half - and establish a regime of shared or separate ownership. In the case of separate ownership, the contract can indicate that “whoever earned what and bought what belongs to him.”

With shared ownership, you can indicate specific shares in the property, for example, that all property will belong to the spouses in a ratio of 70 to 30, or you can register a personal ratio of shares for each type of property.

You can also specify in the marriage contract who will own the property that will appear in the future. For example: all houses purchased in the future will belong to Marina, and cars will belong to Misha.

Price issue

The notary fee for certification of a marriage contract is 500 rubles (current as of the date of writing the article).

You can draw up a standard marriage contract yourself by downloading a sample on the Internet and adjusting it to your requirements. If a homemade database is drawn up in violation of the law, for example, it states that the wife takes the child to school or the husband watches football no more than once a month, the notary will not certify such an agreement. Or he will assure. And it will be invalidated later. It depends on your luck with the notary.

The cost of a well-developed marriage contract ranges from 5,000 rubles from the guys who will download it from the Internet for you, and up to $30,000 from lawyers from international law firms. It all depends on the amount of property and the experience of specialists: to competently draw up a document, you will need a good analysis of the property and financial situation of the spouses and knowledge of all the possibilities of the law to challenge such transactions (yes, a marriage contract is exactly the same transaction as the alienation of property under a contract purchase and sale). The price of the work, by the way, is indicated without taking into account third-party specialists: appraisers and notaries.

Grounds for challenge

To protect assets, a prenuptial agreement must be drawn up in such a way that no one will think that it was drawn up to hide property. Or at least so that it cannot be proven.

What’s good is that now it’s up to those whose rights are allegedly infringed to challenge the contract. Those. It is not Misha who needs to prove that he, without any intent, transferred everything to Marina, but on the contrary - to the creditor or arbitration manager (AM). In any case, to challenge the deal, the stars must converge on the following points:

- the transaction was concluded with the intent to harm the property rights of creditors;

- it has been proven that this same harm was caused;

- at the same time, the spouse was aware that the agreement was concluded with the aim of concealing property, and not out of great love.

We have a separate article on the procedure for challenging transactions in bankruptcy proceedings. In it we clearly showed which transactions, when and how can be challenged. Therefore, we will not dive into details now.

Here are the main hooks that people cling to when challenging a marriage contract:

The imaginary nature of the deal. This is a transaction that is made for show, while in fact no one fulfills its terms. For example, our guys got divorced, Marina, according to the database, received 2 apartments, 2 cars and a business, but in fact all this property is used by her ex-husband. To prove the sham of the transaction, the battle involves analyzing bank accounts, sources of payments for utility bills, surveillance, filming with a video camera, linking car parking fees to specific mobile phone numbers, etc. - in short, the entire arsenal of detective investigation. Similarly, transactions are contested when property is transferred under a power of attorney or purchase and sale agreement without the actual transfer of money.

Signs of insolvency. At the time of concluding the BD, neither spouse should have signs of insolvency. If we imagine that Mikhail, as part of the marriage contract, transferred the apartments, house and business to Marina, and kept only the car for himself, and after 2 months the court accepted the creditors’ statement about Misha’s bankruptcy, then the database can be challenged. The courts do not believe in such coincidences, and they are right to do so. I wouldn't believe it either.

Date of conclusion of the marriage contract. The situation when the couple were married for 20 years, then entered into a prenuptial agreement at the age of 21, and after some time Mikhail files for bankruptcy, arouses suspicion, to say the least. Let us remind you that in the general case, a bankruptcy agreement concluded 3 years before the court accepted the bankruptcy petition can be challenged, and in some cases transactions taken 10 years in advance can also be challenged. Example? Please!

Leave your email and we will send you the latest practice on challenging the database and property division agreements:

Duration of obligations. If debts arose before the signing of the marriage contract, they can be fulfilled both at the expense of the debtor and at the expense of the spouse’s property specified in the marriage contract. For example, what was copied to Marina as part of the database may be given away if Misha’s property turns out to be insufficient. Moreover, it is important to consider that if debts arose before the division of joint property, the agreement cannot infringe the rights of creditors. Including the signed agreement, you need to notify your future opponents.

Size of shares. In one of the recent bankruptcy cases, the AU requested that the database be declared invalid, because according to its terms, the value of the property that went to the wife was 13 (!) times higher than the price of the assets of her debtor spouse. This is about the fact that it won’t be possible to transfer all the property to Marina, so that Misha will then throw up his hands in front of the creditors, saying that there is nothing to take from him. Similar to the liquidity of assets: if Misha retains only shares in a business that has only debts, such a deal may also be challenged.

Reducing the bankruptcy estate. The transaction may be challenged if the terms of the BD lead to a reduction in the bankruptcy estate and cause harm to creditors. Example: Misha took out a loan on himself and paid it off himself, but with the money he received he bought an apartment and registered it entirely in Marina’s name. If they prove that the money went to the needs of the family, then the marriage contract will be invalidated, at least in part of this apartment.

How it happens in practice

Attempts to protect property with the help of a database and other agreements with a spouse are quite often covered with a copper basin. Here is one such example: Irina Trefilova was a member of the Iskra Avigaz company, including replacing the chief accountant and deputy. general director In March 2014, the company issued a loan for several million, for which Irina acted as a guarantor. And in April 2021, Irina entered into a prenuptial agreement with her husband, according to which 4 brick buildings, a garage, an underground parking lot, a plot of land, 3 apartments, one of which is 6-room, became the sole property of Oleg.

In February 2021, the court accepted an application to declare Iskra Avigaz bankrupt - since 2014, the company had accumulated hundreds of millions of debts, and payments came to naught. Considering that it was proven that Irina was the person controlling the debtor (KDL), and even acted as a guarantor for the loan, in April 2018 the creditors got to her. This is where her marriage contract surfaced, in which almost all the property was registered in the name of her husband. In this case, there were a whole bunch of grounds for challenging the database:

- as the chief accountant, Irina knew about Iskra’s debts, which means that the database was concluded with the aim of hiding personal property from creditors;

- the agreement was concluded less than 3 years before the court accepted the application for personal bankruptcy;

- the spouses' shares were distributed disproportionately.

The arbitration court declared the database invalid. Attempts to challenge the decision led nowhere. All authorities agreed with the court's arguments, including the Supreme Court, which confirmed that the courts had every reason to challenge the database and restore the joint ownership regime.

As a result, the property was put up for auction. After everything is sold, the spouse will be given his legal 50% of the proceeds, and the rest will go to pay off creditors.

Statute of limitations

If we are already talking about challenging marriage contracts, then we cannot fail to mention one mega-important point: within what period can it be challenged?

Let's assume a very real situation: the spouses entered into a marriage contract while living in marriage. The husband, understanding in which country he was doing business, stipulated that in the event of a divorce, his wife would receive everything they had acquired together, while he would be left with a donut hole.

After 5 years, the businessman husband receives an application for a subsidy. He urgently gets divorced, triggering the mechanism of division of property. And soon creditors begin to bankrupt him as an individual. Question: is it possible to challenge a marriage contract? And return the property? Let me remind you: the prenuptial agreement was concluded when the business debts were not even visible on the horizon, and 5 years have passed since then.

Correct answer: yes.

To briefly summarize the judicial practice, the statute of limitations in such cases begins to run from the moment the spouse learned that he had lost the right to all jointly acquired property. And this moment coincides with the actual division of property, which began under the terms of the marriage contract only after the divorce.

To receive a similar judicial act, leave your email here:

And so the financial manager, acting on behalf of the husband and in the interests of his creditors, calmly submits an application to invalidate the marriage contract as having created an extremely unfavorable property position in comparison with the wife. And the businessman runs with claims to the would-be lawyers who made him a “very high-quality” prenuptial agreement for as much as 10,000 rubles.

What is important to consider

Yes, protecting personal assets is not a textbook thing to open the night before an exam. Here it is important to understand family law, bankruptcy law, and general trends in the development of judicial practice. And then it becomes quite possible to do this. Here's what you should pay attention to:

A sign of insolvency or insufficient property. It is advisable to conclude any asset protection transactions before signs of insolvency appear for you or your business. If it so happens that difficulties are already visible on the horizon, there is no need to rush headlong into transferring everything to your spouse. In this case, it is important to analyze the value of existing assets and divide them between the spouses so that the terms of the prenuptial agreement are not in doubt.

Notification of creditors. It is important to notify creditors of the signed agreement. This must be done both regarding existing obligations and those arising in the future. In the future, it will be more difficult for the creditor to say that he does not agree with the terms of the database - he was warned. If he didn’t say anything then, let it not arise later.

Date of conclusion of the contract. The court has the right to invalidate a database compiled less than 3 years before the court accepted the bankruptcy petition. And in some cases, even 10 years. Moreover, there is now a practice that courts look differently at contracts concluded before marriage, after a couple of months or after several years. To have as few questions as possible, it is better to enter into a BD before marriage or immediately after registration. The earlier the contract is concluded, the higher its reliability in the eyes of the court.

Distribution of shares. Considering that creditors and insurance companies are fighting for justice, it will not be possible to transfer everything to the spouse, including both kidneys. More precisely, the court will invalidate such a transaction in one click. It is important to take into account that both spouses have property and no one’s interests are infringed. We cannot voice a universal ratio of shares that the court will not find fault with - each case is individual. But you can contact Igumnov Group, and we will analyze your assets and draw up an agreement individually for your situation.

conclusions

- Is it worth getting married at all...?

- It is advisable to conclude a prenuptial agreement before signs of insolvency arise;

- Both existing and future creditors must be notified of the conclusion of the DB;

- You should not transfer all property to one spouse;

- Spending 1-2% of the value of assets on their protection is normal. Don’t push yourself and hire normal professionals;

- If you nevertheless took the path of a prenuptial agreement, then it makes sense to immediately start its execution by dissolving the marriage;

- To be honest, we at Igumnov Group prefer other tools for protecting personal assets. We will talk about them in the following articles.

The information in the article is current as of the date of publication on our website igumnov.group.

To keep abreast of the latest trends in subsidiarity, bankruptcy and protection of personal assets, come and visit us.

__

Igumnova Anna

senior partner of Igumnov Group,

asset preservation expert, litigation lawyer

Specialization: preparation and support of real estate and land transactions in the pre-bankruptcy period. Judicial protection of the interests of a bona fide purchaser. Organization and support of public auctions for the sale of the debtor’s property.

Maternity capital and marriage contract for a mortgage

More than 90% of families who have received the right to maternal (family) capital invest it in purchasing housing, and most often using borrowed funds. How is the issue resolved if maternity capital and a marriage contract are used for a mortgage?

On the one hand, according to Law No. 256-FZ, an apartment purchased with state money is registered as the common shared property of the mother, father and all children, with shares determined by agreement. And if this is a mortgaged apartment, the shares must be registered in the name of the children 6 months after the encumbrance is removed.

When maternity capital is involved in the purchase, a prenuptial agreement for a mortgage eliminates many problems. In it you can:

- indicate the shares of the children - they can be anything, but it is more reasonable to allocate them in an amount proportional to the amount of maternal capital divided among all family members;

- provide for the possibility of appropriate compensation for the share of family capital to a spouse who, during a divorce, loses the right to the purchased apartment.

In the absence of a marriage contract before receiving a loan, this issue has practically no solution. Attempts to go to court to allocate shares to children in a mortgaged apartment lead to refusal, since the bank intervenes, which almost never gives permission for such an allocation, as well as for the sale of an apartment or the division of debt between co-borrowers. In rare cases, courts still consider such cases, but the decision made does not suit everyone. There are two positions.

First approach. Judges divide the apartment in equal shares, for example, ¼ for each of the parents and two children, without taking into account that only part of it was paid for with maternal capital. Reason: Art. 245 of the Civil Code of the Russian Federation, which states that if the shares are not determined by agreement, the property belongs to all applicants in equal shares. The children's shares will belong to the parent with whom they live.

Example. Decision of the Vologda City Court of the Vologda Region in case No. 2-427/2014 (2-12521/2013)~M-11327/2013 dated 01/23/2014.

If the parents are divorced and the mortgage loan will be paid off after dividing the apartment, the children should be allocated shares in the common property acquired using maternity capital funds. Since there is no agreement on the size of shares, and they cannot be determined by law, the shares of the plaintiff, defendant and children are recognized as equal for each.

Second approach. Some judges divide the amount of family capital equally between family members, and if there are supporting documents, they take into account the actual contribution of each spouse. In the Review of the Supreme Court dated June 22, 2016, this position was confirmed. According to the Family Code, parents do not have the right to their children’s property, and the latter to their parents’ property. Therefore, it is fair to divide maternity capital proportionally between all family members, and this equality does not apply to other funds with which the apartment was purchased. Therefore, when drawing up a marriage contract for a mortgaged apartment, it is recommended to adhere to this position.

How to sell an apartment after payment with a marriage contract?

The spouse who has been identified and registered in the marriage contract as the owner of the living space, that is, indicated by the official owner, has the right to sell.

Need to know! It is possible to sell living space in which minors are registered only if the children have been provided with another place of residence and registration.

The same applies to living space purchased using maternity capital, in which young children are registered. Such real estate can be sold if minors are provided with a share of the new housing that is equal in terms of conditions, square footage or exceeds the area (in other cases, the square meters may be less, taking into account the increased amenities of the new place of residence). If children have already reached the age of majority, each of them must consent to the sale.

Distribution of tax benefits and deductions for personal income tax

As a rule, spouses who bought an apartment apply for a tax deduction on income for personal property. You can only receive it for the amount of your own money spent, without taking into account maternity capital. If there are two parties to the purchase and sale agreement, the deduction is provided to each of them in proportion to the share in the property.

How is the issue resolved if a marriage contract is concluded when purchasing an apartment, or subsequently, after the deduction has been processed? The fact is that the federal tax service refused to revise the amount of the deduction after a change in the composition of the owners. The answer is given in the cassation Ruling of the Supreme Court No. 5-KG17-53 (06.06.2017).

So, for example, according to the marriage contract for a mortgaged apartment, it became the sole property of the wife, whereas before its conclusion it was registered in equal shares, and accordingly, each spouse received 50% of the required deduction. The Supreme Court ruled that in this case, along with the apartment and the obligation to repay the loan on it, the right to receive the full amount of the deduction, including interest, passes to the spouse.

The second question arises regarding the determination of the 3-year period of ownership of the apartment, after which the seller is exempt from paying income tax. According to the definition of the Constitutional Court No. 444-O (02.11.2006), the transfer of rights to one of the participants in common property does not entail a change in the period of ownership of the property. Therefore, if, after concluding a marriage contract, the mortgaged apartment passes to one of the spouses, and he intends to sell it, such a transaction will not be subject to personal income tax.

Conclusions. The wider spread of marriage contracts is hampered by stereotypes of a predominantly psychological nature. With its help, you can avoid many problems and conflicts that arise during the division of property, including those encumbered by a mortgage, and resolve issues of repaying a loan after a divorce.

Error two. Specify the property to be divided

Often, spouses who shared shares in commercial organizations by marriage contract do not take into account the possibility of creating new legal entities. The same applies to other movable and immovable property. For example, if the marriage contract specifies a share in Romashka LLC, then the shares in the new legal entities Buttercup LLC and Astra LLC will be jointly owned by the spouses.

The transfer of shares, shares or property to one of the spouses by a marriage contract will not only avoid the need to obtain the consent of the other half for transactions with these assets, but will also prevent a potential corporate conflict. Or even a business stop. After all, the spouse who received part of the share as a result of division can participate in the management of the company, receive any information and documents, and in some cases demand payment of the actual value of the share.

Excessive specification became the businessman’s mistake in the next case. The husband and wife stated in the prenuptial agreement that all gifts received from mutual friends are the joint property of both spouses. Upon divorce, the spouse intended to include the parking space in the common property for division, but the court refused to do so. The wife acquired the parking space on the basis of a gift agreement, and her husband was the donor. Since the marriage contract established a regime of joint ownership only for gifts from friends, the husband's gifts were not included in the common property of the spouses.

To avoid such mistakes, we recommend using general language when describing property in a marriage contract. For example, if only one of the spouses is engaged in business, then the property subject to transfer to his personal ownership should be determined as: shares of participation in business organizations that have already been created or will ever be created; the actual value of these shares to be paid; distributed profit; property of liquidated legal entities remaining after completion of settlements with creditors.