The concept of “business fragmentation” entered our everyday life at the beginning of the 2000s, when legislation was adopted that eased the tax burden of small businesses. They seemed so attractive to businessmen of a larger caliber that they suggested disaggregation. They were not stopped either by potential inconveniences (after all, now, instead of one enlarged structure, they will have to control many small ones, and, moreover, split ones), nor by sharply rising tax risks.

Soon the benefits of this management scheme became so obvious that even once cautious taxpayers began to swell the ranks of those wishing to adopt it.

Let's try to understand the vicissitudes of the issue and understand how legal this kind of business is.

What is business fragmentation?

Naturally, no one in Russia invented a new wheel. Entrepreneurs around the world work successfully and quite legally using a business division scheme, which makes management even more effective, separates production and trading cycles from each other, and reduces business risks.

Speaking about the fragmentation of business in our country, one should understand the realized desire of business entities to minimize their financial results by all permitted and unauthorized means, and, therefore, to reduce tax obligations to the state. For this purpose, they often artificially create local organizations, which, in fact, continue to carry out the same activities as part of the general structure, but enjoy preferential tax regimes.

Such a scheme does not conflict with legislation, in particular tax legislation, if, of course, it is developed taking into account all the pitfalls.

In other words, the “division of property” must be carried out competently and legally, and this task is not always possible to cope with. Sometimes misinterpreting the saying “the end justifies the means,” some business executives reach the point of absurdity when, for example, only a couple of watchmen and cleaners remain on staff at the head office, or the same people are included in the staffing of several, in fact, branches .

Attention! Such an illiterate solution to the problem is perceived with caution by the tax authorities, and subsequently by the judicial authorities.

How to properly split a business

To avoid fines and restrictions, follow these simple rules:

- Rent separate offices for each company.

- Buy both companies their own equipment and machinery.

- Stick to the same tax burden that was before the business split.

- Hire different employees. Each organization must have its own staff of people who cannot work in two companies at the same time.

- Pay taxes and business expenses from your current account.

- Choose different OKVED codes for companies.

Read more about the nuances and rules of doing business in accordance with 115-FZ, which will help you avoid the same mistakes, in the article “How to avoid restrictions on account transactions.”

The “Blocking Risk” service will help you check your business for compliance with the standards of 115-FZ, and you can consult the results of monitoring operations over the last 12 months through the “Compliance Assistant”.

Signs and schemes

The main suspicious signs and schemes that lead tax authorities to think about artificial fragmentation are those in which supposedly completely autonomous organizations:

- have the same leaders in the person of founders and general directors;

- carry out activities at the same legal and physical address, including the use of common contact numbers;

- are serviced by a single personnel and accounting service, when even the same computer is used for reporting;

- freely dispose of the property of a partner (allegedly) organization;

- agree on the provision of mutual services with the free movement of personnel from one organization to another (the institution of part-time work is actively used);

- exchange services that facilitate each other's activities

- using various methods of accounting for expenses and income, they accumulate mutual accounts payable;

- have the same standard delivery notes, invoices and identical contracts with customers or suppliers;

- cash registers are serviced by the same employees;

- use the same logos, presentation brochures, signs, etc.

In addition, illegal optimization is characterized by the absence of a real business plan or a specific business goal. Naturally, in such cases, fragmentation cannot be considered legal.

By the way! Typical violations of legislation relating to taxes and fees are described on the official website of the Federal Tax Service of the Russian Federation.

What business is not subject to division?

According to legal requirements, a business will not be subject to division in the following cases:

- the object of the dispute was opened/received before the marriage was registered;

- the business came into the possession of only one spouse through a non-cash transaction (inheritance, gift).

In this case, only the organization will not share, but the second partner will be able to claim part of the profit.

Example 1:

Citizen K. acquired 10% of the shares before marriage. After registering the marriage relationship, he became the owner of another 20% of the organization’s shares. During the divorce, the spouse of citizen K. filed claims for part of the securities. The court satisfied the request by dividing the shares purchased after marriage between the wife and husband, that is, the wife became the owner of 5% of the shares.

Example 2:

Citizen S. registered an individual entrepreneur before her marriage. During the marriage, her account collected profits from the enterprise, which the couple planned to invest in the purchase of real estate, but divorced before the purchase. When dividing joint property, the court demanded to provide a bank statement with the balance of the corporate account, which contained 9,000,000 rubles. The judge indicated that the profit belonged equally to the spouses, and therefore decided to transfer 4.5 million rubles of profit to the husband.

How to optimize while complying with the law?

Nobody questions the axiom: the main thing in business is making a profit. Another thing is that you need to act with an eye on the legality and proceed from those public and unspoken truths that guide the bodies that supervise economic activities. This case is no exception and requires compliance with several, not so complicated conditions. Let's talk about them in more detail.

- Fragmentation should not be carried out spontaneously, but using competent preliminary preparation. This means correctly understanding the number of future legal entities based on calculations and based on projected revenues for the next year.

- Since the division must follow from the business plan of the enterprise, it is necessary to have such a clear justification for the business goals that they look convincing in the eyes of the fiscal authorities. This presupposes proof of the independence of each of the individual companies: multidirectional activities, possession of its own property and assets, accuracy in staffing. The presence of different addresses, bank accounts, contact information is not even discussed - it is simply necessary! By the way, about bills. The ideal option is when they are opened in various credit institutions.

- Making managerial and financial decisions must be completely independent. At least according to the documents.

- The spin-off organizations must develop real economic activity. Tax officials must be able to convince that each of them strives to obtain real profits using an autonomous pricing policy.

- If problems still exist, they should be justified. For example, if one of the breakaway firms does not have its own premises, the tax authorities (and subsequently, possibly the court) must ensure that the nature of the business allows such an indulgence. Another example: a company may not own a sufficient amount of large equipment, but there should be no problems with furniture, office equipment and other surroundings. There are many similar examples.

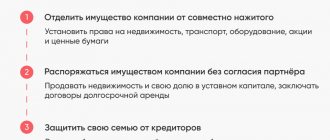

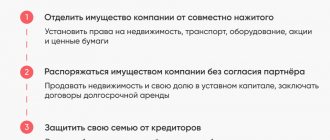

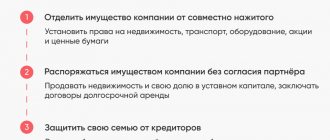

Forms of business division during divorce

The couple needs to resolve division issues in the following areas:

- profit received from commercial activities;

- bonds;

- material goods on the balance sheet of the enterprise;

- IP;

- stock;

- ownership shares in the LLC.

According to the general rule, the business is divided in half between the partners, regardless of who carries out the entrepreneurial activity. A woman housewife claims 50% of the joint property, despite not having a job.

Financial compensation

One of the most convenient ways is to provide monetary compensation. Algorithm:

- The parties invite a specialist to evaluate all property, including assets, profits, debt obligations, and tangible assets.

- Dividing the amount received in half is the legal share of each spouse.

The participants amicably decide who will keep the business after the marriage ends. The spouse who wishes to remain the sole owner offers the other partner a one-time cash payment equal to the legal share. The agreed amount of compensation may differ depending on the conditions agreed upon by the participants. In general, this is like buying part of the second partner's property, but without registering the sale.

You must confirm the transfer of money with a check, bank receipt, or notarized receipt.

Enterprise reorganization

The law provides for the right to reorganize an existing enterprise, which may consist of the following actions:

- merger of several companies;

- dividing one organization into several departments;

- a complete change in production activity.

In the case of division of property during divorce proceedings, couples may decide to reorganize, where the company is divided into 2 separate organizations. One remains under the control of the husband, the second - the wife.

Making decisions on your own is not enough. Additionally, such a decision should be approved by law. Important aspects:

- transmission to the tax service of an initiative letter from the owners to carry out reorganization by dividing the company in half;

- provision of documents by each entrepreneur for the upcoming re-registration of property;

- guarantee of protection of workers' labor rights - people must be notified in writing about upcoming changes at least 2 months before the designated date of reorganization.

The procedure can be carried out during marriage, at the stage of divorce or after receiving a certificate of termination of the marriage.

Sale and liquidation

Termination of a legal entity may be forced or voluntary. A couple running a business together can sell the company or close it, which is accompanied by the sale of all corporate assets. The profit received is divided in half.

The procedure for appointing a new owner is accompanied by the submission of documents to the Federal Tax Service, where changes are made to the Unified State Register of Legal Entities (Unified State Register of Legal Entities). The closure of an organization is also carried out through the tax service.

How is the property of an individual entrepreneur divided when spouses divorce?

Division of property during divorce if there are children

If the legality of the division cannot be proven

In this case, businessmen will face legal proceedings. Of course, it is not a fact that fiscal officials will be able to prove the illegality of optimization in all cases. However, the lack of perfection and clarity of legislation makes the line between legality and illegality very thin.

Of course, the Tax Code of the Russian Federation does not prohibit an entrepreneur from having two or more companies that operate using “imputation” or “simplified taxation,” just as it does not prohibit having a family business. Moreover, in paragraph 7 of Art. 3 of the Tax Code of the Russian Federation especially emphasizes that in case of any contradictions or doubts in the interpretation of legislation on taxes and fees, the decision is made in favor of the legal entity.

In reality, it turns out this way: conducting business activities using several organizations or individual entrepreneurs means arousing the suspicions of tax authorities of deliberate non-payment of all kinds of taxes. This is interpreted as an artificial distribution of revenue using the relationship of legal entities controlled by the parent organization, operating under light tax regimes. This leads to a summary: on the part of the participants in the scheme, there is only an imitation of entrepreneurial activity - in reality, they are under the control of the parent organization. It is in this spirit that employees of the lower echelons of fiscal authorities - those who carry out on-site inspections - are instructed.

Therefore, we should be fair and directly note that if 8-10 years ago judicial practice noted a certain loyalty towards legal entities, today the situation is close to the exact opposite: to win the court when the tax authorities provide what they consider to be strong evidence illegal crushing is practically not considered possible.

Attention! To prevent things from coming to this, only one thing is necessary: to act exclusively within the framework of tax legislation.

How much will you have to pay for violation?

The division of a business while maintaining signs of affiliation for the purpose of extracting tax benefits is qualified by the tax authorities under clause 1 and clause 3 of Art. 122 of the Tax Code of the Russian Federation. The organization must pay a fine, which depends on the amount of unpaid tax and ranges from 20 to 40 percent.

All companies included in the affiliation group may be among the entities subject to punishment. As a measure of responsibility, additional taxes are used when splitting up a business; inspectors have the right to carry out such an action for each legal entity. In this case, the regulatory authorities will have to prove the amount of obligations based on primary documents. Current legislation does not provide for criminal liability for business fragmentation. According to criminal law, qualification under Art. 199 of the Criminal Code of the Russian Federation - tax evasion, then the tax inspector is obliged to send information to the investigative authorities.

Division of company debts

The division of debts that a company has acquired can take place in two ways:

- The spouse who took out the loan will be considered responsible for the debts. It is possible provided that the spouse spent the money received on personal needs, on his own property, etc.

- Debts are recognized as common, and the spouses will both bear responsibility for them in the future. This option is carried out if the funds were spent on business development or the acquisition of common property of the spouses.

A lawyer's answers to questions about the division of business during divorce

Is it possible to sell a business before a divorce and buy it again after the divorce?

No, there is a risk that such a transaction will be declared invalid.

Can I count on a share in the business if I divorce my husband if I did not take part in its creation and management?

If the business is registered after the wedding, then yes.

I am divorcing my husband, he is an individual entrepreneur. We have an adult child, will he have a share in his father's business in a divorce?

No, children, regardless of age, cannot claim the personal and joint property of their parents during a divorce.

Arbitrage practice

When considering business disputes, courts focus on family law. In some cases, an amendment is made to the constituent documents.

But the basic rule remains unchanged. Corporate rights are distributed strictly equally without any exceptions.

Below is a brief description of several use cases. They are specially selected so that it is clear how different types of business are divided.

Division of three LLCs

The citizen filed an application to the court for divorce and division of property from her husband. The list also included shares in three companies registered in the husband’s name.

The Oktyabrsky District Court of Ulan-Ude, by its decision dated July 24, 2020 in case No. 2-551/2020, divided the shares in the authorized capital of all LLCs in half. At the same time, it was noted that the section of corporate rights does not require consent from other participants.

The plaintiff also asked to split the funds in the account of one of the enterprises. This part was refused, since the money belongs to the property of the company.

Property of individual entrepreneurs at the stage of bankruptcy

The bankruptcy trustee of an individual entrepreneur (the owner of a farm) filed a claim against the spouses for the allocation of the debtor's share from the common property. Previously, the arbitration court declared the marriage contract concluded between the defendants invalid.

The plaintiff explained that the defendant’s personal property was not enough to pay off all debts. Therefore, it was decided to foreclose on the share included in the family property.

By the decision of the Birobidzhansky District Court of the Jewish Autonomous Region dated February 13, 2018 in case No. 2-20/2018, the requirements were satisfied in full. The recognition of the claim also played a role.

Shares section

The plaintiff filed a claim against her ex-husband for division of property. The list also included 67.7% of the shares of one of the companies. The defendant admitted claims only for 3 percent of the securities.

During the consideration of the case, it turned out that after the divorce, 64.7% of the shares were sold to a third party without the consent of the citizen. The claim being considered in the arbitration court to invalidate the purchase and sale agreement was not satisfied.

Therefore, the Frunzensky District Court of St. Petersburg, by its decision dated October 16, 2017 in case No. 2-1178/2017, divided the mentioned 3% between the parties. At the same time, the reasoning part states that the wife is not deprived of the right to demand half of what she received from the sale of shares. However, this issue was not raised in the considered claim.