Based:

- Law “On Protection of Consumer Rights”;

- Decree of the Government of the Russian Federation No. 55 of January 19, 1998. (as amended by Decrees of the Government of the Russian Federation No. 1222 of October 20, 1998).

THE FOLLOWING PRODUCTS OF GOOD QUALITY ARE NOT SUBJECT TO EXCHANGE OR RETURN:

1. Medicines

2. Goods for the prevention and treatment of diseases: - sanitary and hygiene items made of metal, rubber, textiles and other materials; — medical instruments, devices, equipment; — oral hygiene products; - spectacle lenses; - child care items. 3. Personal hygiene items

4. Perfume and cosmetic products

What does the Law say?

First, let's define what is considered a food product. According to Articles 492 of the Civil Code and 2 of the Federal Law “On the Fundamentals of State Regulation of Trade Activities in the Russian Federation,” a food product is considered a product that can be consumed, in other words, eaten or drunk.

The return of food (and non-food) goods to a store is regulated by the Law “On the Protection of Consumer Rights”. Thus, according to it, it is impossible to return food products to the store if they are of proper quality (not expired, and must be used for their intended purpose).

So, for example, if you bought Cheddar cheese at the store, and upon arriving home you realized that it does not fit the Caesar salad recipe that you are going to prepare, then return it to the store on the basis of personal antipathy (you just didn’t like it) you will not succeed, since the cheese can be used for its intended purpose, i.e. eat. In a particular case, the seller’s refusal to return the food product will be legal.

However, regarding the return of food products of inadequate quality, according to the Law “On the Protection of Consumer Rights”, it is possible to return them back to the store. In which case? If a food product, for some reason, is not suitable for consumption.

How can I return food products of proper quality?

Food products belong to the type of goods that are legally not subject to exchange or return if they meet quality standards and sanitary standards.

Even if the client just paid for the purchase and decided to immediately refuse it, according to the law he has no right to do so if his requirements are exclusively subjective. After the cash receipt has been punched, refusal of food of proper quality is prohibited.

If the client does not have any evidence that the product does not meet quality standards, then he will have to contact the appropriate organization for an examination, which will either confirm his concerns about the product or refute them. The satisfaction of his requirements will depend on the results of the examination.

How to return products of poor quality?

As we already understood from the previous section, it is impossible to return food products of proper quality to the store. Regarding the return of unusable products, they are returned under the following circumstances:

- Expiration date of the purchased food product;

- Uncharacteristic odor;

For example, purchased cheese smells like mold or rot.

- Uncharacteristic color;

The beige color of baked milk stated on the packaging turned out to be cloudy green.

- Opened packaging;

For example, failure to seal many food products (dairy, meat) can lead to contamination with harmful bacteria and their rapid spoilage.

- Inconsistency between the description of the food product and the “reality” seen;

Information

Example: on the packaging of beef sausages it is written that they have a pronounced purple tint. In fact, they turned out to be pale pink. The buyer has the right to return them to the store on the basis of a discrepancy between what was expected and what was stated.

- The presence of some insects in the purchased food product;

As a rule, the appearance of some kind of “living creatures” in products is due to violations of their transportation and storage conditions in store warehouses.

If one of the listed conditions for return occurs, then such products are subject to return.

Options for returning products of good quality

The main thing is to keep your receipt!

As it became clear from the material presented earlier, no organization that sells them is obligated to accept the return of food products of proper quality. Considering this fact, it is important to understand that such products can only be returned if they are found to not comply with the level of declared or officially defined quality.

In the case of food products, a return due to the reason “does not fit the shape or dimensions” is not possible by law. Despite this, some stores or food stores practice returns and exchanges of food products of any quality. If in your specific case you were lucky and came across a similar organization, then it is quite possible to agree on a replacement or return of products.

However, if a store refuses to receive food products of proper quality back, the blame is solely on itself, since the organization’s management has every right to take such actions. It is worth understanding that if there is any suspicion of inadequate quality of edible products, it is quite possible to return it or exchange it in absolutely any store. In this case, the fact of poor quality or its non-compliance with standards will have to be proven. Evidence is divided into two types:

- The first are obvious arguments in favor of inadequate quality, which are indicated by the buyer and the seller does not deny their presence. If there are such, as a rule, problems with organizing the return or exchange of goods do not arise.

- The second are truthful arguments in favor of inadequate quality, which may be indicated by the buyer, but are not accepted by the seller. Evidence of this kind can only be obtained by conducting an appropriate examination by contacting Rospotrebnadzor. In such situations, it is often impossible to avoid legal disputes with the organization selling the bad product.

In general, in terms of the sale of food products, legislation takes into account the positions and interests of both parties to legal relations: buyers and sellers, equally. If it comes to products of inadequate quality and their return, then the law is completely on the side of the buyer, but if it is necessary to return products of proper quality, the legislator adheres to the position of the seller. For some, such norms may seem unfair, but it is important to adhere to them, because the law is the same for everyone and cannot be violated.

What can a buyer expect?

According to the Law “On the Protection of Consumer Rights”, when returning food products of inadequate quality, the buyer can count on the following actions of the seller:

- Exchange of an unusable food product for a suitable analogue;

- Refund of the full cost of the returned food product in exchange for its return;

- Reducing the cost of a low-quality food product due to revealed unsuitability;

- Compensation for losses incurred;

This item is provided in case, as a result of the unsuitability of a food product, a person suffers a serious illness, which is why he had to undergo long-term treatment. In this case, the buyer may demand that the store compensate for the costs incurred to eliminate signs of poisoning. If the store refuses to pay compensation, then the buyer, according to the Law, can sue the store.

The basis for filing a claim may be an unexpected reaction to a product that a person has consumed.

Information

Example: the packaging of low-lactose cream states that this product is suitable for use by people who are lactose intolerant. After consuming this cream, lactose-intolerant men began to suffer from intestinal upset, which indicates intolerance to low-lactose cream. Conclusion: a man has the right not only to return the cream to the store, but also to demand compensation for the cost of the medicine purchased to eliminate an intestinal disorder.

Return and exchange of goods of inadequate quality

- The Customer may return the Product of inadequate quality to the manufacturer or seller and demand a refund of the amount paid, as well as demand replacement of the Product of inadequate quality or elimination of defects in the event of:

- detection of a significant defect in the product;

- violation of deadlines for eliminating product defects;

- inability to use the product during each year of the warranty period for a total of more than 30 days due to repeated elimination of its various deficiencies.

- If a defect is detected, the Customer returns the Product to the manufacturer or seller. The product must be returned along with the warranty card (if available) and a copy of the Certificate (conclusion) of the Service Center.

- If the Customer returns a Product of inadequate quality, the Seller returns to him the cost of the returned Product no later than 10 days from the date the Seller received the Product of inadequate quality, provided that the defect in the Product is a manufacturing defect and did not arise through the fault of the client.

- Exchange of Goods of inadequate quality is carried out by returning the Goods to the Seller with subsequent cancellation of the Order or Goods, then placing a new Order. In this case, cancellation is a technical action and does not imply the Seller’s refusal to fulfill the contract. The funds are returned to the Client in full. If at the time of the Client’s request a similar Product is not available for sale from the Seller, the Client has the right to refuse to execute the sales contract and demand a refund of the amount paid for the specified Product. The Seller returns the amount of money for the returned Goods within the period established by law.

- When purchasing a set of goods under a promotion in which a discount was provided on one of the goods or all the goods in the set, goods of inadequate quality can only be returned as part of the set. Returns of individual items from a set are not possible unless otherwise provided in the promotion rules.

- The Customer can repair the product of inadequate quality at an authorized service center, or transfer it to the Seller for repairs during the established warranty period for the Product.

What is the step-by-step process for returning?

To return food products of inadequate quality, the buyer will need:

- The food product itself;

- A receipt confirming the purchase of this product;

If the buyer has lost the receipt, this cannot become a basis for refusing to make a return.

- Passport (for filling out a return application);

When you come to the store you should:

- Provide a food product and indicate the reason for its unsuitability;

If the reason for the unsuitability of the product turns out to be, in the seller’s opinion, subjective (implicit), then he will immediately send the product for examination, initially asking you to fill out an application to return the product.

- If the unsuitability of the returned food product is obvious (mold on the cheese, a weathered part of the meat where a hole formed on the package, etc.), then the seller will exchange the low-quality product for a high-quality analogue, reduce the cost of the product or return your money;

- If the seller decides to submit the product for examination, then you will need to fill out a claim;

The seller will provide you with a sample claim. It is compiled in two copies. One copy remains in the hands of the buyer, and the second is sent to the store administration for review.

Return of perishable goods. Accounting with the supplier

Our organization supplies perishable goods to retail chains in the city and region. Stores return spoiled goods. How should we write it off, are there standards and how is it reflected in accounting?

In accordance with paragraphs. "and" clause 2 of Art. 13 Federal Law of the Russian Federation dated December 28, 2009 No. 381-FZ “On the fundamentals of state regulation of trade activities in the Russian Federation”

business entities engaged in trading activities for the sale of food products through the organization of a trading network, and business entities supplying food products to retail chains,

are prohibited from imposing on the counterparty a condition to return to the business entity

that supplied the food products such

goods that were not sold after a certain period of time , except for

cases where the return of such goods is allowed or provided for by the legislation of the Russian Federation.

At the same time, according to the Federal Antimonopoly Service of the Russian Federation, the voluntary inclusion of a return condition

to an economic entity that has supplied food products, such goods not sold after a certain period of time

is not a violation of the prohibition

established by paragraphs. “and” clause 2 of Art. 13 of the Law on Trade (letter dated July 15, 2010 No. IA/22313).

The Ministry of Finance of the Russian Federation believes that if an organization, by agreement with the buyer, accepts an expired product back

, then such an operation should be considered

as a sale of goods

.

That is, the organization (the original seller) becomes the buyer, and the original buyer becomes the seller.

It follows from this that damaged goods are purchased at inflated prices.

, since its cost exceeds the price of the same product, but suitable for further sale, purchased from other suppliers.

Thus, the Ministry of Finance believes, the cost of purchasing goods from the original buyer

in this case, they do not meet the criteria of economic feasibility specified in

Art. 252 of the Tax Code of the Russian Federation

, and

do not reduce the tax base for income tax

(letter dated May 24, 2006 No. 03-03-04/1/475).

However, the Constitutional Court of the Russian Federation

in the Determination of 04.06.2007 No. 320-O-P indicated that

the validity of expenses

taken into account when calculating the tax base

should be assessed taking into account circumstances indicating the taxpayer’s intentions to obtain an economic effect

as a result of real business or other economic activity.

At the same time, we are talking about intentions

and the goals (direction) of this activity,

and not about its result

.

At the same time, the validity of obtaining a tax benefit, as noted in the same Resolution, cannot be made dependent on the efficiency of the use of capital.

Tax legislation does not use the concept of economic feasibility and does not regulate the procedure and conditions for conducting financial and economic activities, and therefore the validity of expenses

that reduce income received for tax purposes

cannot be assessed from the point of view of their expediency, rationality, efficiency or the result obtained

.

In other words, expenses incurred

, including

the repurchase of unsold goods, should not unconditionally lead to the receipt of income

, which the Ministry of Finance insists on.

But for officials, this position of the Constitutional Court of the Russian Federation is apparently not a decree.

And they continue to argue that the cost of purchasing expired goods

cannot be considered as part of the extraction of income from business activities and, therefore,

are not subject to accounting as expenses

for profit tax purposes,

if the obligation to repurchase goods is not established by regulatory legal acts

.

The editors have repeatedly commented on letters from the Ministry of Finance of the Russian Federation on this topic.

One of the latest is letter dated 09/06/2010 No. 03-03-06/1/580.

At the same time, once the financial department unexpectedly expressed a different opinion

.

In a letter dated 07/08/2008 No. 03-03-06/1/397, the Ministry of Finance reported that expenses in the form of the cost of products purchased for the purpose of further sale that are subject to destruction due to the expiration date, as well as expenses associated with the destruction of such products can be taken into account for profit tax purposes, provided

that these expenses were incurred as part of business activities and are properly documented.

But then he again delivered a disappointing verdict

: in the case of disposal (write-off) of expired goods, the costs of their acquisition and further liquidation

cannot be considered as part of the extraction of income

from business activities and, therefore,

are not subject to accounting as expenses for profit tax purposes

.

In accordance with the Federal Law of the Russian Federation dated January 2, 2000 No. 29-FZ “On the quality and safety of food products,”

food products, materials and products

whose expiration dates have expired

cannot be in circulation .

Such food products are disposed of or destroyed

.

Expenses

storage, transportation, disposal or destruction of low-quality and dangerous food products, materials and products

are paid by their owner

.

Resolution of the State Committee for Sanitary and Epidemiological Supervision of the Russian Federation dated September 25, 1996 No. 20 for enterprises of the food and processing industry approved Sanitary rules and standards for the production of bread, bakery and confectionery products SanPiN 2.3.4.545-96.

Based on clause 3.11.8 of the Sanitary Rules, bread and bakery products after the expiration of the sales period are subject to removal from the sales floor and are returned to the supplier as stale

.

The procedure and conditions for returning bread, bakery and confectionery products with cream to the enterprise have also been established.

Thus, the provisions of the Sanitary Rules

:

– the supplier (manufacturer) is held responsible for the processing (disposal) or destruction of low-quality food products, regardless of the fact that the ownership of these food products has transferred to the trade organization, which, taking into account the requirements of Law No. 29-FZ, is the owner of these products;

– predetermines the need to include in contracts for the alienation of bakery industry products (purchase and sale, delivery) to trade organizations a condition on the subsequent purchase of these products by suppliers (manufacturers) after the expiration of the sales period or on the conclusion of agreements on the purchase of low-quality food products for the purpose of their subsequent disposal or destruction.

Thus, the existing regulatory legal regulation of relations in the sphere of turnover of bakery products obliges suppliers (manufacturers) to purchase (repurchase) bread, bakery and confectionery products with an expired shelf life from trading enterprises and carry out their subsequent disposal through processing or destruction.

In this regard, the Ministry of Finance had to agree that expenses in the form of the cost of purchased (redeemed) bakery and confectionery products with expired

suitability of trading enterprises for subsequent disposal by processing or destruction, as well as

expenses associated with the destruction of such products, can be taken into account for profit tax purposes,

provided that these expenses are incurred within the framework of business activities and are properly documented.

At the same time, officials recalled that clause 2 of Art. 3 of Law No. 29-FZ establishes the conditions under which food products, materials and products are recognized as low-quality and dangerous and cannot be sold, disposed of or destroyed.

Thus, when making a decision on the repurchase of products, one should be guided by this norm, taking into account, among other things, the established deadlines for the sale of products

.

However, the absence of these conditions and the expiration of the implementation period

products

are not

grounds

for repurchase of products (letter of the Ministry of Finance of the Russian Federation dated September 14, 2010 No. 03-03-06/1/587).

But, unfortunately, the Ministry of Finance issued such a “positive” conclusion only in relation to bakery products, because the direct instructions of the Sanitary Rules simply cannot be ignored.

For other food products

officials strictly adhere to a firm

“no”

.

Therefore, the likelihood that tax authorities will not accept for tax purposes the costs of purchasing expired goods is very high.

But the chance to defend your right to account for such expenses through the court is also high.

The obligation to repurchase previously delivered goods is assigned to the supplier by the supply agreement

(subject to the voluntary consent of the supplier), which the supplier enters into for the purpose of generating income.

A ban is a ban, and without accepting the condition of repurchasing goods after their expiration date, the supplier would not have been able to conclude this supply agreement at all.

Consequently, the costs of repurchasing goods from the buyer after the expiration date of these goods are economically justified, since the supplier is forced to bear such costs in order to make a profit

.

In judicial practice, there are cases where the courts recognized it as legitimate for the taxpayer to take into account the costs of fulfilling such additional terms of contracts.

In accordance with Part 4 of Art. 20, part 2 art. 25 of Law No. 29-FZ, low-quality food products are subject to appropriate examination carried out by state supervision and control bodies, based on the results of which an authorized person makes a decision on their disposal and destruction.

The procedure for conducting examination of low-quality food products

established by the Regulations on the examination of low-quality and dangerous food raw materials and food products, their use or destruction, approved by Decree of the Government of the Russian Federation of September 29, 1997 No. 1263.

Food products that do not have established expiration dates (for food products for which the establishment of expiration dates is mandatory) or whose expiration dates have expired are subject to withdrawal from circulation, examination, disposal or destruction.

That is, purchased products with expired expiration dates must first be examined and then disposed of or destroyed.

If food products have obvious signs of poor quality

, then it

is subject to disposal or destruction

without examination.

Before disposal or destruction, such products, in the presence of a representative of the state supervision and control body, are denatured by their owner in any technically accessible and reliable way, excluding the possibility of their use as food.

Sampling (samples) of food products subject to examination for laboratory research (tests) is carried out by a representative of state control and supervision authorities in the presence of the owner of the product.

The results of the examination are formalized in the form of a conclusion

, which indicates the non-compliance of food products with the requirements of regulatory documents, and also determines the possibility of its disposal or destruction.

Food Disposal

– is the use of low-quality and dangerous food products for purposes other than the purposes for which the food products are intended.

Food products prohibited for human consumption can be used for animal feed or as raw materials

for recycling or technical disposal.

The owner of such food products, within 3 days after transferring them for use for purposes not related to food consumption, is obliged to submit a document to the state supervision and control body that made the decision on disposal

or a copy thereof, certified by a notary,

confirming the fact of acceptance of the product by the organization carrying out its further use

.

If products cannot be recycled, they must be destroyed.

Destruction of food products

carried out in any technically accessible way in compliance with the mandatory requirements of regulatory and technical documents on environmental protection.

Destruction

destruction of products is carried out

in the presence of a commission

formed by the owner of the product together with the organization responsible for its destruction.

Destruction

food products are documented

in an act

of the established form.

One copy of the act within 3 days

must be submitted to the state supervision and control body that made the decision to destroy it.

As we have already found out, the Ministry of Finance of the Russian Federation prohibits taking into account the costs of disposal and destruction of expired goods for profit tax purposes.

To be fair, it should be noted that the Federal Tax Service of the Russian Federation

holds

a different point of view

.

In a letter dated July 16, 2009 No. 3-2-09/139, answering the question about the accounting procedure for income tax purposes for expenses caused by the withdrawal from circulation of perfumery and cosmetic products and expired household chemicals

expiration date, the Federal Tax Service of the Russian Federation reported that despite the fact that

the operations of destruction of products

by trade organizations in themselves do not correspond to the goals of the activities of a commercial trade organization, the state’s determination of the necessary procedure for such actions in the event of the expiration date of perfumery and cosmetic products and household chemical goods actually

recognizes such operations related to activities aimed at generating income

.

According to the provisions of clauses 15 and 18 of the Regulations on the examination of low-quality and dangerous food raw materials and food products, responsibility for the transfer of products prohibited for consumption for further use or its destruction rests with the owner of the product.

Thus, notes the Federal Tax Service of the Russian Federation, a procedure similar to the above is also applied in the event of withdrawal from circulation of perfumery and cosmetic products and household chemicals with an expired shelf life by their manufacturer.

Since in this case the Federal Tax Service of the Russian Federation referred to the Regulations on the examination of low-quality and dangerous food raw materials and food products, their use and destruction, the tax authorities’ arguments about perfumes and cosmetics products fully apply to food products, which are also named in the Regulations

.

But local tax officials read letters from the Federal Tax Service literally: since the letter deals only with perfumery and cosmetic products, it means that this letter does not apply to other types of products and goods.

Arbitration courts do not agree with officials.

According to the judges, since the operations of destruction of products by trade organizations do not correspond to the goals of the activities of a commercial trade organization, the determination by the state of the necessary procedure in the case when products are subject to destruction actually recognizes such operations as related to activities aimed at generating income

.

Accordingly, compliance by the taxpayer organization with the established procedure is the basis for recognizing expenses caused by the withdrawal of goods from circulation as expenses associated with activities aimed at generating income.

In this case, these expenses are taken into account in reducing the tax base for income tax.

on the basis

of Art. 264 Tax Code of the Russian Federation

.

But at the same time, arbitrators pay attention to the documentation of operations for the disposal and destruction of low-quality food products

, which must be issued in strict accordance with the Regulations.

In case of failure to comply with the established procedure for seizure

from the circulation of food products, disposal operations are not considered within the framework of activities aimed at generating income.

In this case, disposal costs, including the cost of disposed products, are not taken into account in reducing the tax base for income tax, since these costs do not comply with the conditions of Art. 252 Tax Code of the Russian Federation

(see, for example, resolution of

the Federal Antimonopoly Service of the North-Western District

dated 07/06/2009 No. A05-9935/2008).

If, according to the supply contract, ownership

the goods being shipped are transferred to the buyer

at the time of shipment

, then the accounting transactions for the sale and “repurchase” of the goods will be reflected:

DEBIT 62 CREDIT 90

subaccount “Revenue” – revenue from the sale of goods is reflected;

DEBIT 90

subaccount “Cost of sales”

CREDIT 41

– cost of goods sold is written off;

DEBIT 90 CREDIT 68

– VAT reflected.

When returning an expired product:

DEBIT 41 CREDIT 60

– returned goods are reflected;

DEBIT 19 CREDIT 60

– VAT is reflected on returned goods;

DEBIT 60 CREDIT 51

– the cost of the returned goods has been paid;

DEBIT 44 CREDIT 60

– the cost of the examination is reflected;

DEBIT 60 CREDIT 51

– the cost of the examination has been paid.

When disposing of expired goods

:

DEBIT 62 CREDIT 90

subaccount “Revenue” – revenue from the sale of goods for disposal is reflected;

DEBIT 90 CREDIT 41

– the cost of goods sold for disposal is written off;

DEBIT 90 CREDIT 68

– VAT reflected;

DEBIT 68 CREDIT 19

– accepted for deduction of VAT on goods sold for disposal.

Goods for disposal are sold at a significant discount.

The remaining cost of disposed goods is written off to the debit of account 91 subaccount “Other expenses”.

When destroying expired goods.

According to the Chart of Accounts... for shortages and damage to valuables, entries are made by debiting account 94 “Shortages and losses from damage to valuables” from the credit of the accounts accounting for these valuables.

DEBIT 94 CREDIT 41

– goods subject to destruction have been written off;

DEBIT 91

subaccount “Other expenses”

CREDIT 94

– reflects the cost of losses from damage to goods;

DEBIT 91 CREDIT 60 (76)

– reflects the cost of work to destroy expired goods.

the question of VAT deduction simply arises.

.

Officials unanimously declare that the disposal of goods for reasons not related to sales, in particular due to destruction after expiration, on the basis of Art.

39 and 146 of the Tax Code of the Russian Federation

,

is not subject to VAT

.

Therefore, the tax amounts

, previously legally

accepted for deduction

for these goods,

must be restored

.

In this case, the restoration is made in that tax period

, in which goods with an expired shelf life

are deregistered

in the prescribed manner (letters of the Ministry of Finance of the Russian Federation dated November 1, 2007 No. 03-07-15/175, dated July 20, 2009 No. 03-03-06/1/480, Federal Tax Service of Moscow dated November 25, 2009 No. 16-15/123920.1).

Supreme Arbitration Court of the Russian Federation

By decision of October 23, 2006 No. 10652/06, the provisions of the letter of the Federal Tax Service of the Russian Federation, imposing on taxpayers the obligation to contribute to the budget the amounts of VAT previously accepted for offset, not provided for by the Tax Code of the Russian Federation, invalid.

The court indicated that paragraph

3 of Art. 170 of the Tax Code of the Russian Federation provides for cases

in which tax amounts accepted for deduction by the taxpayer on goods (work, services), including fixed assets and intangible assets, property rights,

are subject to restoration

.

A shortage of goods discovered during the inventory of property, or the theft of goods, is among the cases listed in clause

3 of Art. 170 of the Tax Code of the Russian Federation

do not apply.

The majority of federal arbitration courts agree with the position of the Supreme Arbitration Court of the Russian Federation.

For example, FAS Ural District

reminded the tax authorities that, according to

Art.

171 and

172 of the Tax Code of the Russian Federation,

VAT amounts on goods purchased to carry out transactions recognized as an object of taxation are subject to deductions.

To make a deduction, you must have invoices; documents confirming the actual payment of VAT; primary documents confirming the acceptance of goods for registration.

Clause 3 Art. 170 Tax Code of the Russian Federation

provides for cases in which tax amounts accepted for deduction by the taxpayer on goods (works, services), including fixed assets and intangible assets, property rights, are subject to restoration.

Destruction

(damage)

to the goods

to the number of cases listed in

clause 3 of Art. 170 of the Tax Code of the Russian Federation

,

does not apply

.

Thus, the law does not provide

the taxpayer’s obligation

to restore

and pay to the budget tax amounts previously legally claimed for deduction

on goods

purchased for use in transactions recognized as objects of taxation,

but subsequently not used in these transactions due to destruction

(damage) (

resolution dated January 22, 2009 No. Ф09-10369/08-С2

).

Therefore, if you want to deduct VAT when destroying expired goods, then you will have to defend your right in court with almost one hundred percent certainty of victory.

If you do not want to argue with the tax authorities, then the amount of restored VAT should be taken into account in the debit of account 94 as part of losses from damage to valuables.

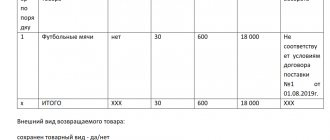

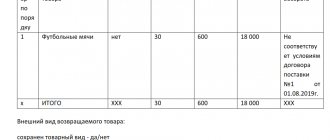

Claim structure

You can fill out a claim both in the store and before going to the store at home. This can be done either on a computer (followed by printing and signing) or by hand. When making a claim, you must adhere to the following structure for writing it:

- On the right side of the A4 sheet, you must indicate the name of the store where the product was purchased (if you know the initials of the director of the outlet, then you must indicate them too). Then the applicant’s personal data is entered: last name, first name, patronymic, residential address, mobile phone number, email address;

- Next, you need to indicate the name of the document, namely “Claim”;

- The main part of the claim must describe in free form: how and when the food product was purchased (its name and cost), under what circumstances its unsuitability was revealed;

- It is necessary to support the information presented with specific articles of the law “On the Protection of Consumer Rights”. Without them, the likelihood of denial of the claims set forth in the complaint may increase;

- At the end, you need to indicate what demands the buyer puts forward in relation to the store: exchange the product, return the money, reduce the cost or compensate for additional costs;

- Next, you need to specify what documents the buyer attaches to the claim. Such documents can be checks.

Documents must demonstrate the facts stated in the claim.

Helpful advice

The claim itself must be accompanied not by original documents, but only by photocopies. Because if lost, they will have to be restored again.

- At the very end of the claim you need to put the date of its preparation, as well as a personal signature with a transcript;

Sample documents

By clicking on the link, you can download the necessary sample documents:

How to write a claim containing a request for a refund for returned products?

In order for the store to consider the issue of exchanging or returning food that does not meet the requirements for quality or other characteristics, the buyer must write a complaint. This document is standard and must be filled out according to a specific template.

It can be handwritten or printed.

The claim includes the document header, title, main text and final part.

In the header of the document, the buyer indicates the addressee of the claim. He must indicate the full name of the store, actual address, full name of the seller or manager. Then he indicates his information as an applicant: full name, actual residential address, contact information.

He then moves on to the title of the document. Here he can select one of the options: “Claim” or “Complaint”.

The main text of the letter includes a detailed statement of the essence of the problem. To begin with, the client must indicate the date and time of purchase of the goods, indicating the place and name of the seller, as well as the cost spent. He then proceeds to state the facts on the basis of which the product should be accepted back or exchanged for similar products.

Application for return of defective goods

Read about returning clothes to the store here.

How to return expired goods to the store, read the link:

References to the legislative framework can increase the chances of a positive consideration of the complaint. Then he lists all the evidence that relates to the issue of the conflict: purchase receipt, photographs of low-quality goods, certificates.

These documents are copied and attached to the claim. Then the client must voice his requirements in detail: a refund in full or in part, or an exchange of goods for another. Next, he indicates the desired time frame for consideration of the claim; the state gives a maximum of a month for this from the date of writing the document. The minimum period for consideration is a week from the date of filing the complaint.

In the final part, the citizen puts the date of drawing up the claim and confirms it with his signature with a transcript.

The claim must be filled out in two copies. The citizen keeps one of them for himself, and the second sends the claim to the addressee. He can submit the claim personally, handing it over to the store manager, or send it by registered mail with notification by mail.

If the store refuses to consider the client’s claim, then he can draw up an appropriate act of violation of his civil rights in the presence of two witnesses, and submit the case to the court.

The seller has a period of from a week to a month to consider the client’s complaint and tell him his decision. Depending on the evidence provided, he can either satisfy the buyer’s demands in full or partially, or refuse him.

If the seller does not make a decision regarding the complaint within thirty days after drawing up the complaint, then the buyer has the right to contact Rospotrebnadzor or the Society for the Protection of Consumer Rights to resolve his issue.