When you provide services or sell goods, you need to register your business activity. Without registration, they can be fined up to 200,000 rubles under Article 14.1 of the Code of Administrative Offenses of the Russian Federation.

Registering a legal entity is difficult: you need a company charter, capital, and a lot of documents for the Federal Tax Service. It’s easier to become self-employed or an individual entrepreneur. Let’s figure out what’s better: registering an individual entrepreneur or registering for self-employment.

Who can register an individual entrepreneur?

Almost anyone can register an individual entrepreneur. There are several restrictions: the legal capacity of the future entrepreneur should not be limited by law or court, he should not be in government or military service. If a citizen has not reached 18 years of age, he can become an individual entrepreneur only in one of the cases:

- He got married.

- He received his parents' consent to start a business.

- There is a decision of the court (or the guardianship and trusteeship authority) on the full legal capacity of the citizen.

Even foreigners and stateless persons can open an individual entrepreneur if they have a temporary residence permit or residence permit in the Russian Federation.

Legal status and characteristics of business entities. Is an individual entrepreneur an individual or a legal entity?

To understand what status an individual entrepreneur has - an individual or a legal entity, let us study the legislative norms that establish the definition of an individual entrepreneur and a legal entity.

According to paragraph 1 of Art. 23 of the Civil Code of the Russian Federation, a citizen can engage in his own business without creating a legal entity. In this case, he will need to obtain individual entrepreneur status.

The exact definition of the essence of IP is contained in paragraph. 4 tbsp. 11 of the Tax Code of the Russian Federation. An individual entrepreneur is an individual registered with the tax authority in the appropriate status and running his own business without forming a legal entity.

Find out how an individual entrepreneur differs from a legal entity in ConsultantPlus. Study the material by getting trial access to the K+ system for free.

Features of a legal entity are given in Art. 48 Civil Code of the Russian Federation. Entity:

- has separate property;

- bears property liability for arising obligations (at the expense of assets belonging to the organization itself, and not to its founder);

- has a registration record in the Unified State Register of Legal Entities.

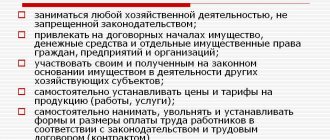

Based on the wording established by the current tax and civil legislation, the answer to the question of whether an individual entrepreneur is a legal entity or not is clear: an individual entrepreneur does not possess the characteristics of a legal entity. The opinion that an individual entrepreneur is a legal entity is erroneous.

IMPORTANT! By registering an individual entrepreneur, a businessman does not lose the status of an individual, carries out business activities on his own behalf and independently bears all the risks that arise in the course of doing business (including at the expense of his own property not used for the development of the business).

Is it possible to register an individual entrepreneur not at the place of registration?

It is possible if you do not have a residence permit (permanent registration). In all other cases, registration of individual entrepreneurs is carried out only at the address of permanent residence indicated in the passport. The tax office is determined at the same address, to which you will need to submit documents for registration, and subsequently reporting.

Even if a citizen is registered in one region and conducts activities in another, registration of an individual entrepreneur and registration with the tax office is still carried out at the place of registration. If you do not have a residence permit, you can register an individual entrepreneur at your place of temporary stay or actual residence, which will have to be confirmed by documents.

Acceptance certificate

An act of provision of services or completed work is a document that the customer and the contractor sign based on the results of the provision of services or completion of work .

Acceptance certificates are important primary documents. They confirm the fact that the service was performed (the work was completed), as well as the fact that the customer accepted them and has no claims against the contractor.

The act is drawn up in two copies and signed by both parties. If the cooperation is long-term and services are provided frequently, the act can be drawn up periodically. For example, the contract is concluded for a year, the service is provided once a week - in this case, the act can be drawn up once a month.

Download the Acceptance Certificate for work performed or services provided

Sample Certificate of completed work

Where to submit documents to register an individual entrepreneur?

Documents for registration of individual entrepreneurs are submitted to the tax office: in person, through a representative or online.

In some regions there are tax inspectorates that only deal with the registration and closure of business entities. For example, in Moscow this is Interdistrict Federal Tax Service No. 46. Having registered an individual entrepreneur, the tax office itself will report the new entrepreneur to the district inspectorate, branches of Rosstat and the Pension Fund.

If there is no separate inspection for registration of entrepreneurs in your region, documents for registration of individual entrepreneurs must be submitted to the regional Federal Tax Service Inspectorate at the place of registration.

What taxes should I pay?

This depends on the tax regime you choose. By default, the general taxation system (OSNO) is applied, which involves the payment of taxes on personal income (NDFL), value added tax (VAT) and property.

In special regimes, which are not available to all individual entrepreneurs, one or two taxes are paid instead of the above. You can find out more in the article “All about tax regimes”.

The choice of taxation system also affects the reporting submission schedule.

When and how can you choose a tax regime?

You don’t need to do anything to select BASIC - it will be applied automatically.

You can switch to UTII within 5 working days from the date of actual start of work by submitting an application to the tax office using form No. UTII-2.

To switch to the patent system, you need to submit an application to the tax office in form No. 26.5-1 immediately along with registration documents or later - 10 days before the start of work on the patent.

To apply the simplified tax system, a notification in form No. 26.2-1 is submitted to the tax office. To immediately work on the “simplified” system, the notification must be submitted along with documents for registration of an individual entrepreneur or within 30 days after actual registration. If you do not meet these deadlines, you will be able to switch to the simplified tax system only from the new year.

Packing list

Invoice is a document that the supplier issues to the buyer when shipping goods .

An invoice is used if an individual entrepreneur sells goods to another entrepreneur or legal entity. When selling to ordinary individuals (not individual entrepreneurs), this document is not issued. A consignment note is drawn up in 2 copies:

- one for the supplier as confirmation of the fact of shipment of the goods ;

- another for the buyer - through it he will receive this product.

Most often, the consignment note is drawn up in the form TORG-12, or its own developed unified form.

Download the Invoice in the form TORG-12

Sample invoice TORG-12

Is it necessary to open a bank account?

No, not necessarily. An individual entrepreneur can receive payment from clients in cash, and pay taxes or pay suppliers by receipt at a bank branch.

Despite this, a bank account is convenient because you can:

- Pay taxes and pay bills through online banking.

- It’s safe to store your money (individual entrepreneurs’ accounts are covered by the deposit insurance system).

In addition, there is a limit for cash payments with other individual entrepreneurs and organizations: no more than 100,000 rubles for each agreement, while there are no such restrictions for non-cash payments.

What is self-employment

Self-employment is a simplified name for the NAP: professional income tax. This is a new tax regime effective from the beginning of 2021. Previously, he worked in four regions of Russia; since July 2020, the regions themselves decide whether to introduce it or not. Now NAP can be issued almost throughout the entire territory of Russia.

NAP is a simplified regime for those who earn money themselves and do not receive a salary from an employer. For those who sell goods, provide services and do not want to bother with reporting. Self-employed people pay only 4-6% tax without mandatory insurance contributions and paperwork inherent in the activities of individual entrepreneurs.

Self-employment can be combined with your main job: for example, you work in security in shifts and sell carved wooden plates as a self-employed person. You only have to pay taxes on income received specifically from the sale of plates. And at work you will continue to pay personal income tax.

Can an individual entrepreneur have employees?

An entrepreneur can hire employees under employment contracts. Limits on the maximum number of personnel are established only by the applicable taxation system. For example, on the simplified tax system or UTII the number of employees should not exceed 100 people, and when working under a patent - 15. If the number of employees exceeds the limit, the individual entrepreneur will lose the right to apply the regime and will have to switch to a general taxation system.

Hiring workers will require the individual entrepreneur to register as an employer with the Pension Fund of the Russian Federation and the Social Insurance Fund. There is no need to do this in advance; the funds will need to be notified when signing an employment contract with the first employee.

Agreement

An agreement is the first document signed by the parties to a transaction. The agreement in its classic form is drawn up on paper in 2 copies and signed by both parties indicating their details. In the contract, the parties stipulate important points of their cooperation :

- The subject, that is, the thing in relation to which the transaction is concluded. For example, an agreement for the sale of a certain product or for the provision of a service.

- The cost of the subject of the contract and the payment procedure.

- Rights, obligations and responsibilities of the seller and buyer.

- The procedure according to which the parties can make changes to the contract, terminate it and resolve any disagreements that have arisen.

The contract does not necessarily have to be in writing. For example, if an individual entrepreneur is engaged in the retail sale of goods, then he, in fact, enters into an oral agreement with each of his customers. The object of this contract is the offered product, the price is its value on the price tag. If the buyer pays for this product, it means he accepts the proposed conditions. The fact of concluding such an agreement is confirmed by issuing to the buyer a cash receipt or a document replacing it.

One of the forms of agreement is an offer - this is a proposal to conclude a transaction sent to an unlimited number of persons. The offer is most often posted publicly, for example, on a website. The fact of payment is considered acceptance of the terms of the contract - acceptance of the offer.

How to pay fixed fees?

Fixed contributions must be paid throughout the existence of the individual entrepreneur. They consist of two parts: mandatory and optional.

The mandatory part of contributions does not depend on the actual receipt of income and is indexed annually. It is important to pay it before December 31 of the current year. Within this period, you can pay as conveniently as possible: in a one-time payment or in installments and at any time of the year. In the year of registration of an individual entrepreneur and in the year of termination of activity, the mandatory contribution is proportional to the number of days during which the status of an individual entrepreneur was valid.

The additional part of the fixed contribution depends on the income received by the entrepreneur without taking into account expenses. An additional contribution is paid in the amount of 1% of the amount of income per year exceeding 300,000 rubles until April 1 of the year following the accounting year.

Temporary suspension of activity (for example, at the preparatory stages of activity or in the case of a seasonal business) does not exempt the individual entrepreneur from paying contributions.

Who and how to notify about the start of activities?

In most cases, there is no need to notify anyone about the actual start of activity. The obligation to report this is provided only for a small list of activities - in order to protect consumer rights.

For example, Roszdravnadzor must be notified about the start of work in the field of social services; when providing transport services, Rostransnadzor must be notified; about the provision of household services and the start of trading activities, Rospotrebnadzor must be notified.

Notifications to regulatory authorities are sent before the start of actual activities.